[The de-funding government so its functions can be privatized, or crippled has been actively pursued for generations now. Perhaps the real benefit of the "blue wave" recent elections will be to restore some sensible oversight to government as Rep. Pascrell describes below.

In this connection here's some practical advice (from Anusar Farooqui aka Policytensor):

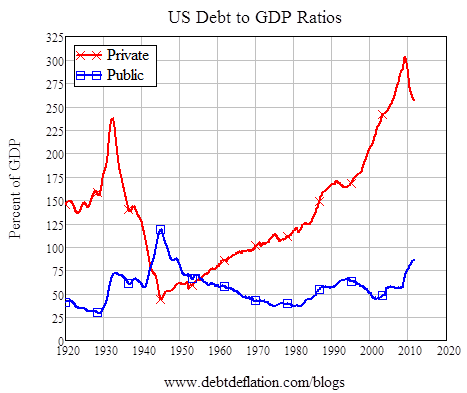

“Doesn’t Minsky offer the connection you seek between the financial cycle and muck? The corruption and swindling is not random but a systematic feature of every mature cycle. One is almost tempted to say it is diagnostic. Like the construction of the tallest building, it makes for an excellent systematic short signal.”] - MD

“Doesn’t Minsky offer the connection you seek between the financial cycle and muck? The corruption and swindling is not random but a systematic feature of every mature cycle. One is almost tempted to say it is diagnostic. Like the construction of the tallest building, it makes for an excellent systematic short signal.”] - MD

By Bill Pascrell Jr. Rep. Bill Pascrell Jr. (D-N.J.) was elected to Congress in 1996. He represents New Jersey's 9th Congressional District.

JANUARY 11, 2019

We lawmakers dumped our in-house experts. Now lobbyists do the thinking for us.

In a year of congressional lowlights, the hearings we held with Silicon Valley leaders last fall may have been the lowest. One of my colleagues in the House asked Google CEO Sundar Pichai about the workings of an iPhone — a rival Apple product. Another colleague asked Facebook head Mark Zuckerberg, “If you’re not listening to us on the phone, who is?” One senator was flabbergasted to learn that Facebook makes money from advertising. Over hours of testimony, my fellow members of Congress struggled to grapple with technologies used daily by most Americans and with the functions of the Internet itself. Given an opportunity to expose the most powerful businesses on Earth to sunlight and scrutiny, the hearings did little to answer tough questions about the tech titans’ monopolies or the impact of their platforms.

It’s not because lawmakers are too stupid to understand Facebook. It’s because our available resources and our policy staffs, the brains of Congress, have been so depleted that we can’t do our jobs properly.

Americans who bemoan a broken Congress rightly focus on ethical questions and electoral partisanship. But the tech hearings demonstrated that our greatest deficiency may be knowledge, not cooperation. Our founts of independent information have been cut off, our investigatory muscles atrophied, our committees stripped of their ability to develop policy, our small staffs overwhelmed by the army of lobbyists who roam Washington. Congress is increasingly unable to comprehend a world growing more socially, economically and technologically multifaceted — and we did this to ourselves.

When the 110th Congress opened in 2007, Democrats rode into office on a tide of outrage at the George W. Bush administration and the Republican Congress, which had looked the other way during the Tom DeLay, Jack Abramoff and Duke Cunningham scandals. My colleagues and I focused our energies on exposing corruption. But we missed crucial opportunities to reform the institution of Congress. As my party assumes a new majority in the House, we confront similar circumstances and have a second chance to begin the hard work of nursing our chamber back to strength.

Our decay as an institution began in 1995, when conservatives, led by then-Speaker Newt Gingrich (R-Ga.), carried out a full-scale war on government. Gingrich began by slashing the congressional workforce by one-third. He aimed particular ire at Congress’s brain, firing 1 of every 3 staffers at the Government Accountability Office, the Congressional Research Service and the Congressional Budget Office. He defunded the Office of Technology Assessment, a tech-focused think tank. Social scientists have called those moves Congress’s self-lobotomy, and the cuts remain largely unreversed.

Gingrich’s actions didn’t stop with Congress’s mind: He went for its arms and legs, too, as he dismantled the committee system, taking power from chairmen and shifting it to leadership. His successors as speaker have entrenched this practice. While there was a 35 percent decline in committee staffing from 1994 to 2014, funding over that period for leadership staff rose 89 percent.

This imbalance has defanged many of our committees, as bills originating in leadership offices and K Street suites are forced through without analysis or alteration. Very often, lawmakers never even see important legislation until right before we vote on it. During the debate over the Republicans’ 2017 tax package, hours before the floor vote, then-Sen. Claire McCaskill (D-Mo.) tweeted a lobbying firm’s summary of GOP amendments to the bill before she and her colleagues had had a chance to read the legislation. A similar process played out during the Republicans’ other signature effort of the last Congress, the failed repeal of the Affordable Care Act. Their bill would have remade one-sixth of the U.S. economy, but it was not subject to hearings and was introduced just a few hours before being voted on in the dead of night. This is what happens when legislation is no longer grown organically through hearings and debate.

Congress does not have the resources to counter the growth of corporate lobbying. Between 1980 and 2006, the number of organizations in Washington with lobbying arms more than doubled, and lobbying expenditures between 1983 and 2013 ballooned from $200 million to $3.2 billion. A stunning 2015 study found that corporations now devote more resources to lobby Congress than Congress spends to fund itself. During the 2017 fight over the tax legislation, the watchdog group Public Citizen found that there were more than 6,200 registered tax lobbyists, vs. 130 aides on the Senate Finance Committee and the Joint Committee on Taxation, a staggering ratio approaching 50-to-1 disfavoring the American people. In 2016 in the House, there were just 1,300 aides on all committees combined, a number that includes clerical and communications workers. Our expert policy staffs are dwarfed by the lobbying class.

The practical impact of this disparity is impossible to overstate as lobbyists flood our offices with information on issues and legislation — information on which many lawmakers have become reliant. Just a few weeks ago, at the end of the session, I witnessed the biennial tradition of departing members of Congress relinquishing their suites to the incoming class. As lawmakers emptied their desks and cabinets, the office hallways were clogged with dumpsters overflowing with reports, white papers, massaged data and other materials, a perfect illustration of the proliferating junk dropped off by lobbyists.

Congress remade its committees in the 1970s to challenge Richard Nixon’s presidency and move power to rank-and-file lawmakers. Many segregationist chairmen were ousted and replaced by reformers, and committees and subcommittees were given flexibility to study issues under their purview. It’s no accident that some of the most significant legislation and oversight by Congress — Title IX; the Clean Water Act; the Watergate, Pike and Church hearings — came from this period. Congress had strengthened its pillars, hired smart people and accessed the best information available.

Following the reforms of the 1970s, the House held some 6,000 hearings per year. But eventually, the number of House hearings fell — from a tick above 4,000 in 1994 to barely more than 2,000 in 2014. On the tax-writing Ways and Means Committee, of which I am a member, oversight hearings are virtually nonexistent, as is developing legislation. We had no hearings in 2017 on the bill that would dramatically rewrite our tax code. And in the last Congress, we didn’t haul in any administration officials for a single public hearing on the renegotiation of the North American Free Trade Agreement. Assessing this state of affairs in a 2017 report, the Congressional Management Foundation noted that committees “have been meeting less often than at almost any other time in recent history.” This neglect has become the norm. Instead, leadership, lobbyists and the White House decide how to solve policy problems.

Indeed, Congress has allowed the White House to dominate policymaking. Trade is a perfect illustration. Despite our current president’s braggadocio, most Americans would be surprised to learn ultimate trade power rests with Congress. But over and over we’ve willingly, even eagerly, handed off that responsibility given to us by Article I, Section 8 of the Constitution. President Trump’s power to renegotiate NAFTA was granted by Congress, as was his power to issue tariffs, allowed under the Trade Expansion Act of 1962. I disagreed with the decision in 2015 to give President Barack Obama — a member of my own party — fast-track power to advance the Trans-Pacific Partnership. During that debate, I sat stupefied as some members of our committee sought to award not only Obama but also future, unknown executives an extended and open-ended authority to make other deals. Congress was prepared to simply abdicate our job.

Perhaps the most striking instance of political interference I’ve seen in my career occurred in the Ways and Means Committee in 2014. Then-Chairman Dave Camp (R-Mich.) had toiled for months with Democrats, Republicans and budget experts to craft a comprehensive tax reform bill. I may not have loved the final product, but I respected the process. Republican leadership killed the proposal almost immediately after it was unveiled. The reason? They wanted to deny Obama a legislative accomplishment.

For decades, nearly every piece of legislation would reach the floor via committee, but beginning in the 1990s, the rate began to drop. In the 113th Congress, approximately 40 percent of big-ticket legislation bypassed committees. Before 1994, Camp would have informed the speaker of his proposal and brought it to the floor. Now, a chairman has much less power to realize meaningful legislation. Meanwhile, longstanding House rules have essentially blocked the amendment process on the floor, meaning bills can’t be modified by members of the wider chamber.

In addition to committee weakness, House lawmakers collectively employ fewer staffers today than they did in 1980. Between 1980 and 2016, when the U.S. population rose by nearly 97 million people and districts grew by 40 percent on average (about 200,000 people per seat), the number of aides in House member offices decreased, to 6,880, and total House staff increased less than 1 percent, to 9,420.

The first lobe of Congress’s brain we can bulk back up is the Congressional Research Service. The CRS provides studies from talented experts spanning law, defense, trade, science, industry and other realms. Some of our greatest oversight triumphs — Watergate, Iran-contra, the Freedom of Information Act — were achieved with the CRS’s support. Great nations build libraries, and much of the CRS is housed in the Library of Congress’s Madison Building.

But the CRS has become a political target. In 2012, a CRS report finding that tax cuts do not generate revenue enraged my Republican colleagues, who had the report pulled and began browbeating CRS experts. According to figures supplied by the CRS, the next year, the service saw its funding cut by $5 million, nearly 5 percent, recovering to previous levels only in 2015. (The CRS did get big funding bumps in recent years.)

The Congressional Budget Office and the Government Accountability Office, crown jewels of our body that provide nonpartisan budget projections, are similarly ignored or maligned for partisan purposes. Last year, when the CBO debunked claims that the GOP tax plan would create jobs, Republicans savaged the agency instead of improving the law. It reminded one of my colleagues, Rep. Jim Himes (D-Conn.), of an episode of “The Simpsons” in which Springfield residents, rescued from a hurtling comet, resolve to raze the town observatory.

The GAO also furnishes rich information to Congress on virtually any subject. Last year I requested and obtained a study on the live-events ticket market. It was a probing report with fresh data. Former senator Tom Coburn (R-Okla.), one of the most conservative lawmakers of the past generation, praised the GAO, estimating that every dollar of funding for the agency potentially saved Americans $90. Nonetheless, from 1980 to 2015, GAO staffing was cut by one-fifth.

While I never had the pleasure of collaborating with the Office of Technology Assessment, its reputation is legendary. Like the GAO, it operated as a think tank for Congress, tasked with studying science and technology issues. The OTA was Congress’s only agency solely conducting scholarly work on these issues until Gingrich disemboweled it. Today, few members of Congress know it ever existed.

The congressional hearings on big tech showcased my colleagues’ inability to wrap their heads around basic technologies. But our challenges don’t stop at Silicon Valley. Biomedical research, CRISPR, space exploration, artificial intelligence, election security, self-driving cars and, most pressingly, climate change are also on Congress’s plate.

And we are functioning like an abacus seeking to decipher string theory. By one estimate, the federal government spends $94 billion on information technology, while Congress spends $0 on independent assessments of technology issues. We are crying out for help to guide our thinking on these emerging areas. I have backed motions to bring the OTA back to life, and I was heartened last year when the House Appropriations Committee approved funding for a study on the feasibility of a new OTA.

The creation in the House rules of a Select Committee for the Modernization of Congress in this new session is a terrific beginning — and a signal that Speaker Nancy Pelosi (D-Calif.) and Rules Committee Chairman Jim McGovern (D-Mass.) understand the importance of these issues. Providing capital and staff to the institution should be a major priority in the 116th Congress. The budgets we approve fund 445 executive departments, agencies, commissions and other federal bodies. But for every $3,000 the United States spends per American on government programs, we allocate only $6 to oversee them.

After decades of disinvesting in itself, Congress has become captured by outside interests and partisans. Lawmakers should be guided by independent scholars, researchers and policy specialists. We must recognize our difficulties in comprehending an impossibly complex world. Undoing the mindless destruction of 1994 will take a lot of effort, but with investment, we can make Congress work again.