This has a little unecessarily juvenile humor, but is spot on, otherwise...

Thursday, April 28, 2022

Sunday, April 24, 2022

Truth, the first casualty of war

Remember this?...

A group of Ukrainian border guards were stationed on Snake Island, in the Black Sea south of Odessa, when a Russian warship ordered them to surrender under threat of attack.

— Alejandro Alvarez (@aletweetsnews) February 25, 2022

Their response: "Russian warship, go fuck yourself."

They held their ground. All 13 were killed. pic.twitter.com/GMRsXQRSX0

That's the furthest thing from the truth. Among others, Huffingtonpost corrects the record here.

In a bizarre bit of counter-intuitive commentary, the Huffpo commenters pretty

much agree the Russians are responsible for this bit of disinformation.

More from the Wikipedia entry "Attack on Snake Island":

Reporting

Ukrainian government sources initially stated that 13 border guards, representing the entirety of the Ukrainian military presence on the island, were killed after refusing to surrender.[21][22] The State Border Guard Service of Ukraine later announced that the guards might instead have been captured,[23] based on Russian reports that they were being held as prisoners of war in Sevastopol.[24]

Russian defense media presented an alternate version of events, claiming that 82 Ukrainian soldiers were taken prisoner after surrendering voluntarily.[13] Russian ministry spokesman Igor Konashenkov claimed that the prisoners have been signing pledges promising not to continue military action against Russia and will be released soon.[25]

On

28 February 2022, the Ukrainian Navy posted on its Facebook page that

all the border guards of the island were alive and detained by the

Russian Navy.[26][27]

Meanwhile, those charitable enough to help the Ukrainians could also help the Yemenis, the Palestinians, the Syrians, the Iraqis, the Hondurans, etc. where the U.S. has either attacked or funded/armed the attackers. And yes, help Ukrainians, where the U.S. did plenty to provoke the inexcusable attack.

To me, the real solution is to lobby Washington to stop demanding Ukraine join NATO, stop arming Ukraine (Trump's contribution) and stop backing out of disarmament treaties (again: Trump).

Friday, April 22, 2022

The Perfect Answer To Sanctimonious Bigotry

Senator Lana Theis accused me by name of grooming and sexualizing children in an attempt to marginalize me for standing up against her marginalizing the LGBTQ community...in a fundraising email, for herself.

— Mallory McMorrow (@MalloryMcMorrow) April 19, 2022

Hate wins when people like me stand by and let it happen. I won't. pic.twitter.com/jL5GU42bTv

Wednesday, April 20, 2022

Orthodox Economics is Bunk - Inflation edition

(c) by Mark Dempsey

Americans tend to treat the pseudo-science called "economics" with the kind of reverence medieval peasants reserved for sacred relics. Yet that same orthodox economics gives intellectual cover to some of the worst public policies, including the sacred (unregulated) market's dog-eat-dog predatory competition that's supposed to turn out best for everyone if the state would just get out of the way. Despite the fact that in all of human history, economic markets have never existed without states to encourage and regulate them.

Orthodox economics failed to predict the largest economic event in 80 years--the subprime/derivatives meltdown, now called the "Global Financial Crisis" or GFC. Students of economics have even protested the "Don't Look Up," tunnel vision allegiance of orthodoxy has to its fundamental assumptions. Harvard economist Greg Mankiw's classes have been staging walkouts because of this bias.

Orthodox economics also informs the decisions of our central bank (The Federal Reserve, or "the Fed"). One example would be its response to the inflation that stems from shortages thanks to COVID and port logjams. That policy is...wait for it...raising interest rates. Yep. That'll cure COVID and unjam the ports. Not even the 19th-century belief that bleeding patients would cure them is as disconnected from the actual problem as the Fed's proposed inflation remedy.

Modern money theorists like Stephanie Kelton often hear criticism that the policies MMT recommends--like a job guarantee--would be inflationary, but MMT always includes resource availability in its spending prescriptions. Besides, government buys surplus soybeans, why not surplus labor? But then...it's not orthodox economics, so being kind to labor isn't "respectable."

Orthodox economics even informs recent inflation reporting, ignoring the asset-price inflation that has been going on for years without too many alarming headlines to announce it. Stock market and housing prices have been on a steady uptrend thanks to public policies orthodox economics blesses like Quantitative Easing, and the Wall Street bailout.

When Wall Street's subprime mortgages and derivatives proved toxic to the banksters who created them in 2007-8, the Fed provided $16 - $29 trillion in credit to make sure the big banks did not fail. Paying off everyone's mortgage would only have taken $9 trillion, but it was economic orthodoxy that made sure Wall Street got the gold mine while Main Street got the shaft.

Without that Fed intervention, the constant asset price inflation we've experienced in recent years would almost certainly have been interrupted by the bankruptcy of several large financial institutions. Sheila Bair, the Republican-appointed head of the FDIC said one recipient of Fed largesse, Citigroup, was insolvent, yet the Fed lent them the money they needed to weather the GFC. Some people believe that the Fed underwote those trillions in loans, but it's one of the first rules of underwriting not to lend to the insolvent. That bailout was a gift, made respectable by orthodox economics.

So the next time you read something claiming "economic studies say..." or "most economists agree," you need to take that policy recommendation with a lot more than a grain of salt, if not disregard it entirely. And remember: orthodox economics is bunk.

Recommended further reading Debunking Economics: The Naked Emperor Dethroned by Steve Keen (who correctly predicted the GFC)

[I'm not the only one who thinks this way, either: “Leading active members of today’s economics profession… have formed themselves into a kind of Politburo for correct economic thinking. As a general rule—as one might generally expect from a gentleman’s club—this has placed them on the wrong side of every important policy issue, and not just recently but for decades. They predict disaster where none occurs. They deny the possibility of events that then happen. … They oppose the most basic, decent and sensible reforms, while offering placebos instead. They are always surprised when something untoward (like a recession) actually occurs. And when finally they sense that some position cannot be sustained, they do not reexamine their ideas. They do not consider the possibility of a flaw in logic or theory. Rather, they simply change the subject. No one loses face, in this club, for having been wrong. No one is disinvited from presenting papers at later annual meetings. And still less is anyone from the outside invited in.” [emphasis added] - from James K. Galbraith’s Who are these economists anyway?]

Update: Why would MSM emit so much propaganda about inflation?

Answer: Corporate profits have contributed disproportionately to inflation. The article includes recommendations for policy makers' responses--things like "stop blaming labor costs." Excerpt:

"Since the trough of the COVID-19 recession in the second quarter of 2020, overall prices in the NFC sector have risen at an annualized rate of 6.1%—a pronounced acceleration over the 1.8% price growth that characterized the pre-pandemic business cycle of 2007–2019. Strikingly, over half of this increase (53.9%) can be attributed to fatter profit margins, with labor costs contributing less than 8% of this increase. This is not normal. From 1979 to 2019, profits only contributed about 11% to price growth and labor costs over 60%"

A little graphic clarity from the same source:

Update #2: (from Ian Welsh)

What Economics Gets Wrong (Almost Everything)

Economics as a discipline is nearly worthless. What it teaches mostly isn’t true.

- Decreasing price does not always increase demand and increasing price sometimes increases demand.

- People do not optimize utility (by any definition that is not circular).

- People are not rational.

- The market is not rational.

- The market does not discount the future well at all.

- Competitive markets are created by government, and destroyed by private actors.

- Markets do not and never have properly priced externalities and never will do so while humans remain human. The only way to price externalities properly is thru government or custom (government in drag.)

- Profit or loss in any enterprise in a modern economy is a social choice, entirely based on government and social decisions and mostly unrelated to fundamentals like energy in and energy out.

- Railroads are far more efficient, energy wise than roads, but govt. subsidizes roads.

- The vast majority of profit is based on market position and sustained profit is almost always based on having an unfair advantage that makes the market less competitive and therefore not have the virtues of competitive markets.

- Genuine competitive markets don’t exist, and no businessman wants them to because they drive profits to almost zero.

- The best economies the world ever saw went out of their way to keep wages and prices high, not to reduce them.

- Any concentration of market power that is not regulated or broken up will engage in practices intended to buy/undermine government and destroy wages.

- Higher CEO pay is correlated with lower company performance.

- You cannot have a good economy for long without keeping the rich poor, weak and under your thumb. It is impossible.

- Monetary efficiency between countries is bad. It should be hard to move large amounts money in and out of another currency or country.

- Financial market efficiency is generally bad, and effectiveness and shock pads should be optimized for rather than financial efficiency.

- Countries should, if it is possible, make or grow everything important inside their own borders and not trade for it.

- People perform better when happy, healthy and at least moderately autonomous. The literature on this is so abundant it is silly. Bosses are authoritarian assholes because they like being authoritarian assholes who micro-manage employees. It’s what Bezos gets out of being Bezos.

- Private money creation concentrated in a few hands is destructive to the economy, democracy and freedom (authority: Thomas Jefferson). It is also anti-competitive market, since you can’t compete with people who create money out of thin air.

- Moderate levels of inflation are good, not bad, if they include assets, because they take away the control of people who won the past so they don’t control the present and the future.

- Taxes should be low on ordinary people and high on anyone rich, including wealth and estate taxes. No one should be rich because their parents were.

- People who lend money should lose that money if the person who they loaned it to can’t afford to repay it. The function of lending is “I know how to pick people who will use the money well.” If you can’t do that you deserve to lose the money, and govt shouldn’t collect it for you

- bankruptcy should be easy, fast and leave people whole. Economically crippled people are not in the interest of society as a whole.

- A UBI’s main function is allowing people to do what they want to do, and forcing bosses to make jobs good, not shitty.

- Pensions should simply be handled by government or a general UBI.

- Comparative advantage is a terrible strategy for improving your economy.

- Free trade is garbage for most countries.

- Raising the minimum wage is not correlated with increased unemployment

- The unemployment rate measures supply driven wage push inflation pressure, not how many peole can’t get a job.

- Initial capital for capitalism was primarily acquired by theft, first of European commons, then of non-European land, people and resources.

Essentially everything Economics teaches is wrong. If and when their prescriptions for action are followed, disaster ensues. With almost no exceptions every country which ever developed did so by not doing what economists say to do.

Economics also has a morally corrosive affect on those who study it. People mostly don’t free rude or otherwise act according to the maxims of economics: but people who have studied economics do.

Because economics is wrong and harmful about almost everything, and because economists do not say “please don’t follow our advice”, Economics should probably be banned and all Economics faculties shut down.

Tuesday, April 19, 2022

Pretty disturbing betrayals by big tech

...go to Twitter to read the whole, very long thread.1. Here's Apple CEO Tim Cook today arguing that antitrust laws against big tech are bad for privacy and bad for national security. In honor of his speech, I thought I'd do a little thread on just how bad these tech firms are for American security. pic.twitter.com/bTdqZ0Sr9d

— Matt Stoller (@matthewstoller) April 12, 2022

Wednesday, April 13, 2022

From Historian Gary Gerstle's Interview with The Nation - What's the domestic significance of the fall of the U.S.S.R?

Excerpted from here.

One consequence of communism’s fall is obvious: It opened a large part of the world—Russia and eastern Europe—to capitalist penetration. It also dramatically widened the willingness of China (still nominally a communist state) to experiment with capitalist economics. Capitalism became global in the 1990s in a way it had not been since prior to the First World War. The globalized and capitalistic world that dominated international affairs in the 1990s and 2000s is unimaginable apart from communism’s collapse.

Another consequence of communism’s fall may be less obvious but is of equal importance: It removed what had been an imperative in America (and in Europe and elsewhere) for compromise between elites and the working classes. A nation once “lost” to communism would never be regained for the capitalist world (or so it was thought). The specter of communist advance impelled capitalist elites in advanced industrial countries, including the United States, to compromise with their class antagonists in ways they would not otherwise have done. A fear of communism made possible the class compromise between capital and labor that underwrote the New Deal order. American labor was strongest when the threat of global communism was greatest. The apogee of America’s welfare state, with all its limitations, was coterminous with the height of the Cold War. After 1991, the year of the Soviet Union’s dissolution, the pressure on capitalist elites and their supporters to compromise with the working class vanished. The dismantling of the welfare state and the labor movement marched in tandem with communism’s collapse.

To argue for communism’s importance is not meant to rehabilitate it as a political movement. Communism was an indefensible system of tyranny. Rather, it is meant to help us to understand the role that communism played in the century when it was a feared force, and then to call on us to reckon with the effects of its sudden and complete disappearance from international and national affairs.

The fall of communism manifested itself not just in the collapse of the Soviet Union but also in the erosion of the emancipatory dreams that had animated leftist movements for 200 years, since the days of the French Revolution. How could one sustain one’s belief in revolution when the greatest experiment in socialist transformation had failed so spectacularly?

(Could the tale of How China Escaped Shock Therapy [by Elizabeth Weber] provide an alternative to empower workers?)

Monday, April 11, 2022

Friday, April 8, 2022

More Federally-mandated Local Guidelines for Climate Safety

In reporting the congressional investigation into recent record oil

company

profits ($70.5 billion in 2021) the L.A. times quotes Amy Myers Jaffe,

energy expert at the Fletcher School at Tufts University saying "The

easy way to pay less for gasoline is to use your car less." It's

statements like this from the professors that make "It's academic" into a

synonym for "It's trivial."

Apparently, Ms. Jaffe is unfamiliar with the design of most U.S. cities since the 1950s. Different uses--commerce, residences, offices, etc.--are separated by car trips. If you want to shop, work (non-remotely), or go to school, you must drive.

If the U.S.

wanted climate safety and respected the "law of holes"--when you want to get out of a hole,

stop digging--it would mandate a return to traditional civic design

that mixes those different uses in single neighborhoods and doesn't

connect them exclusively with collector streets. Street design would

also permit comfortable pedestrian presence there too ("Complete Streets").

How could federal regulations accomplish that? It's surprisingly simple: stop financing the sprawl that requires those car rides for every trip of any significance. Federally-managed institutions' (Fannie Mae [FNMA] and Freddie Mac [FHLMC]) underwriting standards determine the configuration of most homes that are finance-able.

You may be

familiar with Frank Lloyd Write's mandate for architecture: "Form

follows function." Reality dictates current architects and city planners

follow the mandate "Form follows finance."

Changing these institutions' underwriting standards to require pedestrian-friendly mixed-use would prevent the entire nation from building sprawl in new development. Removing sprawl as a possibility would cut vehicle miles traveled, and greenhouse gases generated in newly built neighborhoods roughly in half.

As a bonus, such traditional neighborhoods would even support transit, and fully-utilized mass transit generates roughly one-eighth of the greenhouse gas single-occupant autos produce. Sprawl makes transit virtually impossible since the number of customers within range of the stops is smaller, and the walk to those stops is at least undignified, if not impossible.

Would the market accept such an alternative design? In Sacramento, the most valuable real estate in the region is around McKinley Park, just such a pedestrian-friendly, mixed-use neighborhood. We could even redevelop existing malls to include residences, which could provide more affordable housing, would provide transit hubs, and have higher per-square-foot sales than conventional malls. Current brick-and-mortar commercial development is in economic peril, thanks to the internet and the pandemic.

The change in city design would be a win for all concerned. How many of us even know this possibility exists?

Tuesday, April 5, 2022

How to have fun

this dog knows how to have fun in all kinds of weather

— theworldofdog (@theworldofdog) April 4, 2022

(jukin media) pic.twitter.com/CUEUkoAeQC

Sunday, April 3, 2022

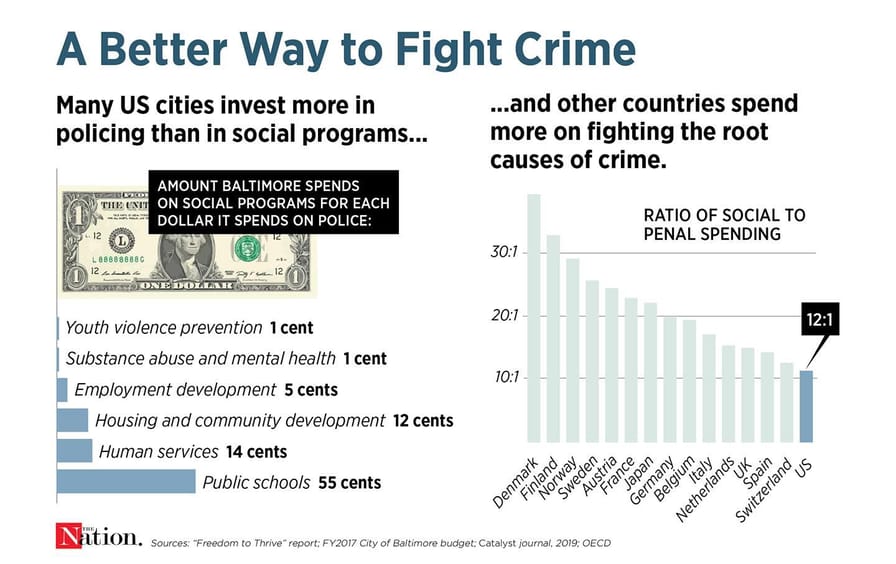

The true crime story

THREAD: There’s a lot of talk right now about crime in San Francisco. Almost everything you’ll read in the mainstream press is wrong. I live in the Tenderloin and work in the courts every day. Here’s my take on what’s happening and why.

— Peter Calloway (@petercalloway) April 1, 2022

Let’s start with an example of the pervasive disinformation: In a recent piece on the TL—where I’ve lived for 4 yrs, and the epicenter of the city’s homelessness and drug crises—a Washington Post journalist, @PostScottWilson, tells readers that crime in the TL is out of control.

— Peter Calloway (@petercalloway) April 1, 2022

Murder and rape are up double-digit percentages since last year! Well, he’s right about that. And it sounds scary. But what are the actual increases (# of incidents, not %)? Homicides increased from 10 to 11. Rapes increased from 22 to 28. https://t.co/uomhDaMBGP

— Peter Calloway (@petercalloway) April 1, 2022

What about crime in the city overall? If you read the Chronicle (with some exceptions), or the recall campaign literature, or national outlets advancing the conservative claim that SF is a failed experiment in progressive policymaking, you probably think it’s out of control.

— Peter Calloway (@petercalloway) April 1, 2022

Let’s take a look at the actual numbers.

— Peter Calloway (@petercalloway) April 1, 2022

First, a note on methodology: These statistics are generated from data provided by SFPD, so we’re playing on their field. And I’m using 2019 as a baseline. Why?

Because in 2020, crime across the country reached historic lows. So while the city saw increases in crime (mostly marginal) in *some* of these categories from 2020-2021, that’s largely due to the fact that for most of 2020, everyone was spending most their time at home indoors.

— Peter Calloway (@petercalloway) April 1, 2022

Now, the numbers: Citywide, from 2019-21, homicides increased 36%. That sounds significant, but the actual # increase was 15. SF has one of the lowest homicide rates among major cities in the US. Include rural communities, and San Francisco’s not even in the conversation.

— Peter Calloway (@petercalloway) April 1, 2022

Over the same period, rape, robbery, and assault *decreased* by 47% (-191), 27% (-851), and 6% (-160). So, violent crime (which the SFPD categorizes as homicide, rape, robbery, and assault) decreased by 19% (-1187). Property crime over that period is down by 11% (-6083).

— Peter Calloway (@petercalloway) April 1, 2022

etc, etc, etc.

Meanwhile, from Northern CA:

(from the Davis Vanguard) Note that Sacramento's DA is no fan of progressive policies. In recent elections, she's opposed every measure to reduce prison populations. As Ankita Joshi writes this week, the irony is that the two DA’s being recalled potentially – George Gascon in LA and Chesa Boudin in San Francisco, have actually done better on a whole host of measures than DA Anne Marie Schubert of Sacramento, who has become the spokesperson for tough on crime policies, both as DA and now running against AG Rob Bonta.

Update (5/21/22):

From this story.

Subscribe to:

Posts (Atom)

Replying to the Anti-Steyer Campaign

About Steyer: He's a billionaire, but endorsed by Bernie Sanders. Talk about odd political bedfellows! Not mentioned: Becerra's don...

-

© by Mark Dempsey In the year 2000 the World Health Organization (WHO) ranked countries’ health care system outcomes according to thin...

-

Here's a detailed explanation by a Modern Monetary Theory founder, Stephanie Kelton. The bottom line: Social Security's enabling l...

-

(c) by Mark Dempsey Blaming current conditions on traditions Ronald Reagan began, or the racist Republicans, as Jeffrey Sachs does (here...