“Only puny secrets need protection. Big discoveries are protected by public incredulity.” - Marshall McCluhan

Although many people treat it like a commodity--a lump of gold, for one example--money is actually (and historically) a measurement, more like the score at the ballgame or the inches on a ruler. It’s a way to keep track of obligations. It evaluates debt; it is an IOU amount and marker.

If, rather than cash, you accept an IOU from a neighbor who is buying your lawn mower at your garage sale, then use the IOU to satisfy a debt with another neighbor, that IOU amounts to a “money thing.” It has both purchased goods and paid off debt. The IOU measures or tracks the obligation(s) throughout the process, and makes the transaction more precise. As economist Hyman Minsky used to say: “Everyone can make money; the problem is getting it accepted.”

Perhaps the most common money technology is checking accounts. When we have such an account it is our asset, but to the bank, it is a liability (an IOU or a debt). When you write a check, you’re assigning a portion of the bank’s liability to the payee. The assets and liabilities are exactly the same item; which one is which depends on one’s perspective (bank or depositor).

This is true for the currency in your wallet, too. Dollars are, in effect, checks made out to “cash” in fixed amounts, drawn on the Federal Reserve (AKA “the Fed,” the United States’ central bank). The Fed carries currency on its books as a liability just as your bank carries your checking account as its liability. Banks also have liabilities for interest-bearing savings accounts and the Fed has an equivalent to such accounts in T-bills and Treasury bonds.

The sum of all dollar financial assets in circulation in the economy therefore equals, to the penny, the national “debt” (a word written in quotes because it is so different from household debt). That statement is not exotic economics; it’s double-entry bookkeeping.

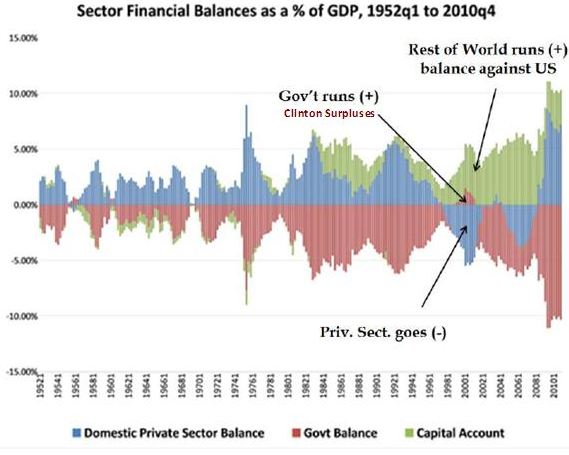

Here’s an illustration of sectoral balances over the years (liabilities are below the line, assets are above):

(This divides the private sector into Domestic and “Capital Account”--i.e. Foreign trade, too)

Clearly assets and liabilities mirror each other. This means, as mentioned above, national “debt” is completely unlike household debt; it’s like bank debt, or household asset.

Even so, the marketing of panic about national “debt” is widespread and well funded. We’re constantly told national “debt” is like household debt. For just one example, Obama compared the federal budget’s deficit to credit card debt.

But no one ever goes to their bank to demand it shrink the amounts in checking accounts, or to say that the bank’s debt is going to crush their grandchildren, and would the bank please diminish its own liability (i.e. the depositors’ assets in their accounts) by increasing its fees or decreasing the interest paid on savings accounts. That would be crazy.

Nevertheless, Pete Peterson and other billionaires are funding think tanks, “Fix the Debt” speaking tours and the like. Local congressman Ami Bera sponsored a Peterson-funded Concord Coalition “Budget Workshop” to poll participants about the best ways to decrease national “debt”--in other words to decrease the population’s assets we call “savings.”

What happens historically when the population plays the “Fiscal Responsibility™“ con game, and significantly reduces national “debt”? The last time this occurred was the Clinton surplus. The previous time such a reduction occurred was in 1929. Andrew Jackson actually paid the “debt” off in 1835. There are seven such major “debt” paydowns since 1776. What happens 100% of the time is that these fits of “Fiscal Responsibility™“ are followed by Great Depression-sized holes in the economy, the worst of which was the Panic of 1837.

The disastrous economic fallout from reducing the population’s assets makes some sense, too. Creditors don’t say “There are fewer dollars in circulation, so we’ll forgive this month’s mortgage payment.” No, they say “Pay your payment or we’ll take your house.” So diminishing the population’s savings in dollar financial assets crushes debtors, and leads to waves of asset forfeitures and foreclosures. Vulture capitalists like Pete Peterson profit mightily from such events, but most ordinary citizens don’t.

There are two other surprising corollaries to the observation that the money government spends and leaves in the economy (rather than retrieving it in taxes) is the population’s asset, not household debt:

Sovereign, fiat currencies (dollar, yen, pound, but not euro) do not provision the governments that issue them. They can’t. Where would taxpayers get the dollars with which to pay taxes if government didn’t spend them out into the economy first? The notion that currency creators must wait for tax revenues to fund programs is really just deflation and austerity promoted in service to vulture capitalists. “Pay as you go” is plausible for households (currency users), but not for governments who are currency creators. It’s practically a logical tautology to say you cannot pay taxes until you have the dollars spent by government, but you’ll hear “tax and spend,” rather than the more accurate “spend, then tax” whenever you listen to mainstream pundits.

While taxes don’t pay for (federal) government programs, they are necessary, however, to make the money valuable. The promised payoff implied by currency is that it will retire those inevitable future tax obligations. Taxes make the money valuable; they don’t provision the (federal) government. Currency is really just tax credits.

The Federal government makes the money and does not need yours. If you went to the Treasury building in Washington D.C. and paid your income taxes in cash, after marking your bill “paid,” Treasury would shred the dollars. They don’t need your money, and make as much as they need whenever policy makers ask for it. Witness the aftermath of Lehman’s bankruptcy when, according to its own audit, the Fed pushed $16 - $29 trillion out the door in 2007-8. (More accurately: they permitted that $16-$29 trillion to be overdrawn in the financial sector’s accounts at the Fed.)

No one ever says “Hey, we’re out of money” when it comes to a war or bank bailouts, public officials only say that for social and environmental programs.

For more information:

See Randall Wray’s piece about the status and history of U.S. Federal “debt” here.

For a comprehensive look at the clever way Italians are side-stepping their monetary non-sovereignty as part of the European Union, see an account of how they are paying people with tax credits. (Never underestimate an Italian!)

For even more details, try Warren Mosler’s Seven Deadly Innocent Frauds of Economic Policy, a 35-page pamphlet that’s available free online.

No comments:

Post a Comment

One of the objects if this blog is to elevate civil discourse. Please do your part by presenting arguments rather than attacks or unfounded accusations.