The election of Donald Trump alerted

many to what should have been obvious long ago: the U.S. economy has

failed to deliver the goods to the vast majority of American families for decades.

In the context of Trump’s election, this economic failure was often

characterized as being unique to white working-class voters in the upper

Midwest. But this is wrong. Income growth has been sluggish, and hourly wage growth near zero,

for low- and middle-income families across the board. The fact is, our

economy has generated enough income in recent decades to deliver very

substantial wage gains for all workers—men and women, people of color

and whites. Our economy has the capacity to provide not just decent

wages but labor protections that support strong families and policies

that provide security in retirement. These charts show the gap between

what is and what could be. (For policies to close the gaps, see EPI’s Real agenda for working people.)

{kind=link}

{kind=link}

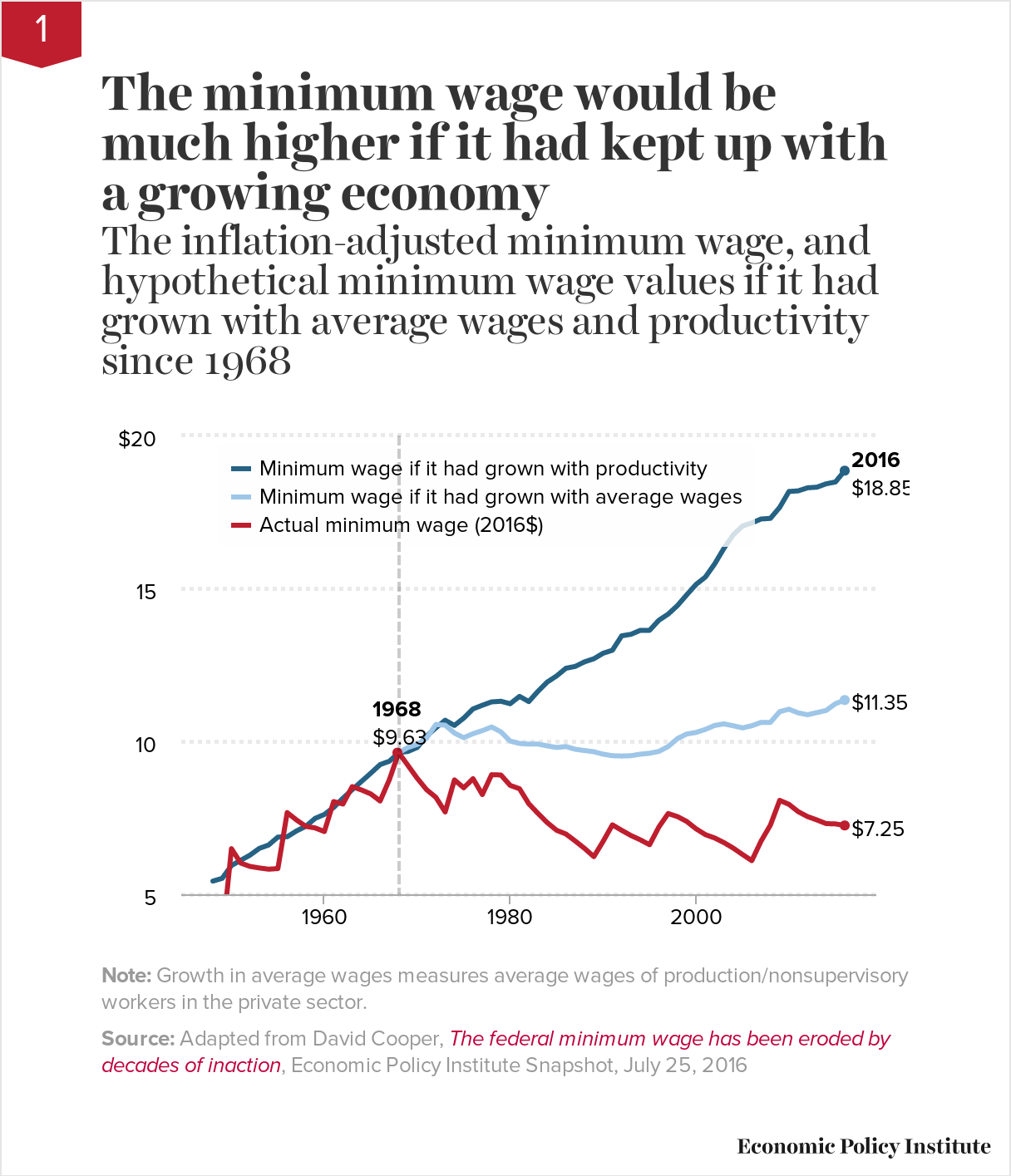

The minimum wage would be much higher if it had kept up with a growing economyThe inflation-adjusted minimum wage, and hypothetical minimum wage values if it had grown with average wages and productivity since 1968

1

| Actual minimum wage (2016$) | Minimum wage if it had grown with average wages | Minimum wage if it had grown with productivity | |

|---|---|---|---|

| 1938 | $ 3.67 | ||

| 1939 | $ 4.46 | ||

| 1940 | $ 4.43 | ||

| 1941 | $ 4.22 | ||

| 1942 | $ 3.81 | ||

| 1943 | $ 3.59 | ||

| 1944 | $ 3.53 | ||

| 1945 | $ 4.60 | ||

| 1946 | $ 4.24 | ||

| 1947 | $ 3.71 | ||

| 1948 | $ 3.46 | $5.43 | |

| 1949 | $ 3.51 | $5.52 | |

| 1950 | $ 6.49 | $5.94 | |

| 1951 | $ 6.02 | $6.11 | |

| 1952 | $ 5.91 | $6.28 | |

| 1953 | $ 5.86 | $6.50 | |

| 1954 | $ 5.82 | $6.61 | |

| 1955 | $ 5.84 | $6.87 | |

| 1956 | $ 7.67 | $6.88 | |

| 1957 | $ 7.43 | $7.07 | |

| 1958 | $ 7.22 | $7.22 | |

| 1959 | $ 7.17 | $7.48 | |

| 1960 | $ 7.05 | $7.61 | |

| 1961 | $ 8.03 | $7.84 | |

| 1962 | $ 7.95 | $8.14 | |

| 1963 | $ 8.52 | $8.42 | |

| 1964 | $ 8.41 | $8.69 | |

| 1965 | $ 8.28 | $8.96 | |

| 1966 | $ 8.05 | $9.24 | |

| 1967 | $ 8.75 | $9.35 | |

| 1968 | $ 9.63 | $ 9.63 | $9.63 |

| 1969 | $ 9.21 | $ 9.80 | $9.67 |

| 1970 | $ 8.79 | $ 9.90 | $9.80 |

| 1971 | $ 8.42 | $ 10.10 | $10.17 |

| 1972 | $ 8.17 | $ 10.55 | $10.44 |

| 1973 | $ 7.69 | $ 10.53 | $10.69 |

| 1974 | $ 8.74 | $ 10.27 | $10.52 |

| 1975 | $ 8.48 | $ 10.12 | $10.76 |

| 1976 | $ 8.78 | $ 10.25 | $11.06 |

| 1977 | $ 8.26 | $ 10.35 | $11.18 |

| 1978 | $ 8.91 | $ 10.47 | $11.29 |

| 1979 | $ 8.90 | $ 10.31 | $11.31 |

| 1980 | $ 8.56 | $ 10.01 | $11.23 |

| 1981 | $ 8.45 | $ 9.93 | $11.47 |

| 1982 | $ 7.96 | $ 9.91 | $11.30 |

| 1983 | $ 7.64 | $ 9.91 | $11.64 |

| 1984 | $ 7.34 | $ 9.85 | $11.94 |

| 1985 | $ 7.09 | $ 9.80 | $12.14 |

| 1986 | $ 6.97 | $ 9.83 | $12.39 |

| 1987 | $ 6.74 | $ 9.74 | $12.45 |

| 1988 | $ 6.50 | $ 9.70 | $12.60 |

| 1989 | $ 6.23 | $ 9.66 | $12.70 |

| 1990 | $ 6.73 | $ 9.58 | $12.88 |

| 1991 | $ 7.27 | $ 9.53 | $12.98 |

| 1992 | $ 7.09 | $ 9.52 | $13.45 |

| 1993 | $ 6.92 | $ 9.53 | $13.50 |

| 1994 | $ 6.78 | $ 9.58 | $13.63 |

| 1995 | $ 6.62 | $ 9.61 | $13.63 |

| 1996 | $ 7.20 | $ 9.67 | $13.96 |

| 1997 | $ 7.64 | $ 9.83 | $14.16 |

| 1998 | $ 7.54 | $ 10.09 | $14.44 |

| 1999 | $ 7.38 | $ 10.24 | $14.79 |

| 2000 | $ 7.14 | $ 10.29 | $15.13 |

| 2001 | $ 6.95 | $ 10.39 | $15.37 |

| 2002 | $ 6.84 | $ 10.52 | $15.80 |

| 2003 | $ 6.69 | $ 10.57 | $16.31 |

| 2004 | $ 6.51 | $ 10.51 | $16.75 |

| 2005 | $ 6.30 | $ 10.44 | $17.04 |

| 2006 | $ 6.10 | $ 10.51 | $17.14 |

| 2007 | $ 6.74 | $ 10.62 | $17.27 |

| 2008 | $ 7.26 | $ 10.62 | $17.29 |

| 2009 | $8.07 | $ 10.97 | $17.65 |

| 2010 | $ 7.94 | $ 11.05 | $18.17 |

| 2011 | $ 7.70 | $ 10.93 | $18.19 |

| 2012 | $ 7.54 | $ 10.87 | $18.29 |

| 2013 | $ 7.43 | $ 10.94 | $18.31 |

| 2014 | $ 7.31 | $ 11.01 | $18.42 |

| 2015 | $ 7.30 | $ 11.23 | $18.48 |

| 2016 | $7.25 | $11.35 | $18.85 |

Note: Growth in average wages measures average wages of production/nonsupervisory workers in the private sector.

Source: Adapted from David Cooper, The federal minimum wage has been eroded by decades of inaction, Economic Policy Institute Snapshot, July 25, 2016

The federal minimum wage is meant to

ensure a fair wage for the nation’s lowest-paid workers. But it hasn’t

done that since 1968. Since the inception of the federal minimum wage in

1938, Congress has periodically raised it, ostensibly so that its real

(inflation-adjusted) value would reflect changing economic

circumstances. Before 1968, the real value of the federal minimum wage

grew at roughly the same pace as the growth in labor productivity—i.e.,

the rate at which the average worker can produce income from each hour

of work. This makes sense: if the economy as a whole can produce more

income per hour of work, it means there is capacity for wages across the

distribution to grow at a similar rate. But after 1968, when the real

value of the minimum wage in today’s dollars was $9.63, the minimum wage

stopped rising at the same pace as productivity. As the top line in the

graph shows, had the minimum wage kept pace with rising productivity,

it would be nearly $19 per hour today. Not $7.25.

This is only one way in which policymakers have failed to ensure that the lowest-paid Americans get their fair share of economic growth and improving labor productivity. As the middle line in the figure shows, if, since 1968, the minimum wage had even just been raised at the same growth rate as average hourly wages of typical U.S. workers, the minimum wage would be $11.35 today. To sum up, minimum wage workers are falling behind not only productivity growth but typical worker pay growth and pay growth of their 1968 counterparts! And as the next chart shows, typical workers (measured here as the nonsupervisory production workers who constitute roughly 80 percent of all private-sector U.S. workers) themselves are lagging behind highly paid supervisors and executives when it comes to claiming a share of economic growth.

This is only one way in which policymakers have failed to ensure that the lowest-paid Americans get their fair share of economic growth and improving labor productivity. As the middle line in the figure shows, if, since 1968, the minimum wage had even just been raised at the same growth rate as average hourly wages of typical U.S. workers, the minimum wage would be $11.35 today. To sum up, minimum wage workers are falling behind not only productivity growth but typical worker pay growth and pay growth of their 1968 counterparts! And as the next chart shows, typical workers (measured here as the nonsupervisory production workers who constitute roughly 80 percent of all private-sector U.S. workers) themselves are lagging behind highly paid supervisors and executives when it comes to claiming a share of economic growth.

{kind=link}

CEOs make 276 times more than typical workersCEO-to-worker compensation ratio, 1965–2015

2

| Year | CEO-to-worker compensation ratio |

|---|---|

| 1965/01/01 | 20.0 |

| 1966/01/01 | 21.2 |

| 1967/01/01 | 22.4 |

| 1968/01/01 | 23.7 |

| 1969/01/01 | 23.4 |

| 1970/01/01 | 23.2 |

| 1971/01/01 | 22.9 |

| 1972/01/01 | 22.6 |

| 1973/01/01 | 22.3 |

| 1974/01/01 | 23.7 |

| 1975/01/01 | 25.1 |

| 1976/01/01 | 26.6 |

| 1977/01/01 | 28.2 |

| 1978/01/01 | 29.9 |

| 1979/01/01 | 31.8 |

| 1980/01/01 | 33.8 |

| 1981/01/01 | 35.9 |

| 1982/01/01 | 38.2 |

| 1983/01/01 | 40.6 |

| 1984/01/01 | 43.2 |

| 1985/01/01 | 45.9 |

| 1986/01/01 | 48.9 |

| 1987/01/01 | 51.9 |

| 1988/01/01 | 55.2 |

| 1989/01/01 | 58.7 |

| 1990/01/01 | 71.2 |

| 1991/01/01 | 86.2 |

| 1992/01/01 | 104.4 |

| 1993/01/01 | 111.8 |

| 1994/01/01 | 87.3 |

| 1995/01/01 | 122.6 |

| 1996/01/01 | 153.8 |

| 1997/01/01 | 233.0 |

| 1998/01/01 | 321.8 |

| 1999/01/01 | 286.7 |

| 2000/01/01 | 376.1 |

| 2001/01/01 | 214.2 |

| 2002/01/01 | 188.5 |

| 2003/01/01 | 227.5 |

| 2004/01/01 | 256.6 |

| 2005/01/01 | 308.0 |

| 2006/01/01 | 341.4 |

| 2007/01/01 | 345.3 |

| 2008/01/01 | 239.3 |

| 2009/01/01 | 195.8 |

| 2010/01/01 | 229.7 |

| 2011/01/01 | 235.5 |

| 2012/01/01 | 285.3 |

| 2013/01/01 | 303.1 |

| 2014/01/01 | 301.9 |

| 2015/01/01 | 275.6 |

Note:

CEO annual compensation is computed using the “options realized”

compensation series, which includes salary, bonus, restricted stock

grants, options exercised, and long-term incentive payouts for CEOs at

the top 350 U.S. firms ranked by sales. Typical worker compensation

refers to annual compensation of the workers in the key industries of

the firms in the sample.

Source: Adapted from Figure C in Lawrence Mishel and Jessica Schieder, Stock market headwinds meant less generous year for some CEOs, Economic Policy Institute Report, July 12, 2016

The compensation of the CEOs of the

largest firms has grown much faster than stock prices, corporate

profits, and the wages of the top 0.1 percent. But the most dramatic

difference is between the compensation of CEOs and the compensation of

typical workers. From 1978 to 2015, CEO compensation grew 941 percent

compared with just 10 percent for the compensation of a typical worker

(annual compensation of the workers in the key industries represented by

the sample).

The figure illustrates the gap in pay between CEOs and employees by tracking the ratio of CEO compensation to that of the typical worker. CEOs of major U.S. companies earned 20 times more than a typical worker in 1965; this ratio grew to 59-to-1 by 1989, and then it surged in the 1990s, hitting 376-to-1 by the end of the 1990s recovery, in 2000. The two stock market crashes after 2000 reduced CEO stock-related pay and caused CEO compensation to tumble. But by 2014, the stock market had recouped all of the value it lost following the 2008 financial crisis and the CEO-to-worker compensation ratio was back to 302-to-1. A dip in the stock market and the value of associated stock options led to a decline in CEO compensation in 2015 and, correspondingly, the CEO-to-worker pay ratio fell to 276-to-1, similar to what happened in other stock market declines at the start of the new millennium and during the Great Recession. Though the CEO-to-worker compensation ratio remains below the peak values achieved earlier in the 2000s, it is far higher than it was in the previous four decades.

The figure illustrates the gap in pay between CEOs and employees by tracking the ratio of CEO compensation to that of the typical worker. CEOs of major U.S. companies earned 20 times more than a typical worker in 1965; this ratio grew to 59-to-1 by 1989, and then it surged in the 1990s, hitting 376-to-1 by the end of the 1990s recovery, in 2000. The two stock market crashes after 2000 reduced CEO stock-related pay and caused CEO compensation to tumble. But by 2014, the stock market had recouped all of the value it lost following the 2008 financial crisis and the CEO-to-worker compensation ratio was back to 302-to-1. A dip in the stock market and the value of associated stock options led to a decline in CEO compensation in 2015 and, correspondingly, the CEO-to-worker pay ratio fell to 276-to-1, similar to what happened in other stock market declines at the start of the new millennium and during the Great Recession. Though the CEO-to-worker compensation ratio remains below the peak values achieved earlier in the 2000s, it is far higher than it was in the previous four decades.

{kind=link}

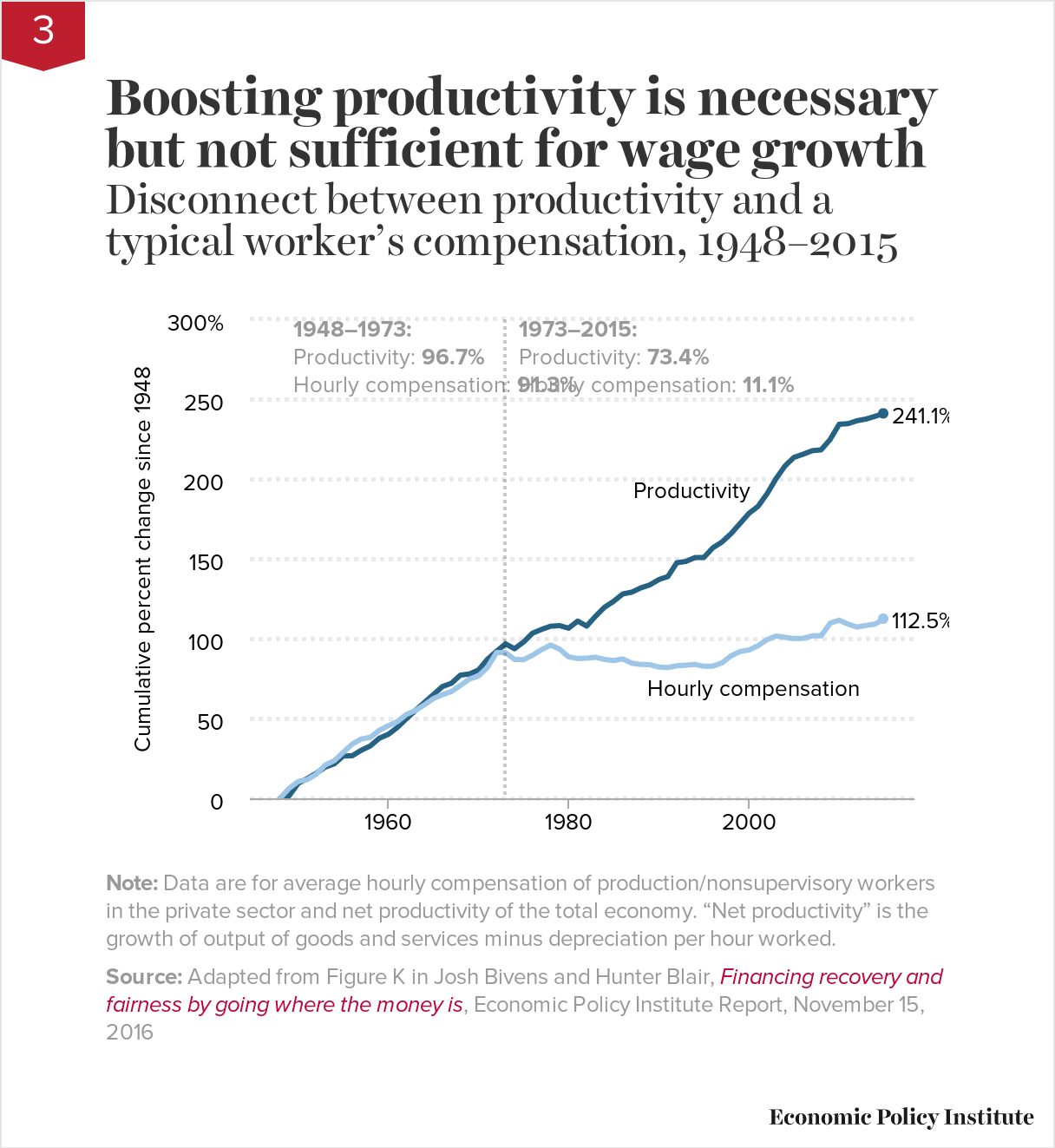

Boosting productivity is necessary but not sufficient for wage growthDisconnect between productivity and a typical worker’s compensation, 1948–2015

3

| Year | Hourly compensation | Net productivity |

|---|---|---|

| 1948 | 0.00% | 0.00% |

| 1949 | 6.25% | 1.55% |

| 1950 | 10.48% | 9.33% |

| 1951 | 11.75% | 12.35% |

| 1952 | 15.04% | 15.63% |

| 1953 | 20.84% | 19.55% |

| 1954 | 23.52% | 21.56% |

| 1955 | 28.74% | 26.46% |

| 1956 | 33.94% | 26.66% |

| 1957 | 37.14% | 30.09% |

| 1958 | 38.16% | 32.78% |

| 1959 | 42.55% | 37.64% |

| 1960 | 45.49% | 40.05% |

| 1961 | 47.99% | 44.36% |

| 1962 | 52.47% | 49.79% |

| 1963 | 55.02% | 55.01% |

| 1964 | 58.50% | 59.99% |

| 1965 | 62.46% | 64.94% |

| 1966 | 64.89% | 70.00% |

| 1967 | 66.89% | 72.05% |

| 1968 | 70.73% | 77.16% |

| 1969 | 74.66% | 77.88% |

| 1970 | 76.59% | 80.37% |

| 1971 | 82.01% | 87.10% |

| 1972 | 91.24% | 92.05% |

| 1973 | 91.29% | 96.75% |

| 1974 | 86.96% | 93.66% |

| 1975 | 86.84% | 97.92% |

| 1976 | 89.66% | 103.44% |

| 1977 | 93.13% | 105.79% |

| 1978 | 95.96% | 107.79% |

| 1979 | 93.43% | 108.14% |

| 1980 | 88.56% | 106.57% |

| 1981 | 87.59% | 111.02% |

| 1982 | 87.76% | 107.88% |

| 1983 | 88.35% | 114.13% |

| 1984 | 86.94% | 119.73% |

| 1985 | 86.31% | 123.43% |

| 1986 | 87.32% | 127.99% |

| 1987 | 84.59% | 129.12% |

| 1988 | 83.85% | 131.78% |

| 1989 | 83.70% | 133.65% |

| 1990 | 82.22% | 136.98% |

| 1991 | 81.87% | 138.89% |

| 1992 | 83.04% | 147.56% |

| 1993 | 83.38% | 148.37% |

| 1994 | 83.82% | 150.75% |

| 1995 | 82.70% | 150.86% |

| 1996 | 82.79% | 156.92% |

| 1997 | 84.80% | 160.50% |

| 1998 | 89.17% | 165.71% |

| 1999 | 91.92% | 172.08% |

| 2000 | 92.90% | 178.50% |

| 2001 | 95.56% | 182.84% |

| 2002 | 99.38% | 190.72% |

| 2003 | 101.63% | 200.17% |

| 2004 | 100.84% | 208.21% |

| 2005 | 100.05% | 213.58% |

| 2006 | 100.21% | 215.48% |

| 2007 | 101.70% | 217.70% |

| 2008 | 101.71% | 218.24% |

| 2009 | 109.69% | 224.75% |

| 2010 | 111.53% | 234.28% |

| 2011 | 109.06% | 234.67% |

| 2012 | 107.27% | 236.51% |

| 2013 | 108.32% | 237.57% |

| 2014 | 109.13% | 239.30% |

| 2015 | 112.53% | 241.08% |

Note: Data

are for average hourly compensation of production/nonsupervisory

workers in the private sector and net productivity of the total economy.

“Net productivity” is the growth of output of goods and services minus

depreciation per hour worked.

Source: Adapted from Figure K in Josh Bivens and Hunter Blair, Financing recovery and fairness by going where the money is, Economic Policy Institute Report, November 15, 2016

The root cause of the extraordinary rise

in inequality and the near-stagnant growth of wages for typical workers

over most of the past generation is the pay-productivity gap. Before

the late 1970s, wages of the vast majority of workers grew in line with

productivity. In the late 1970s, typical worker pay growth split from

economy-wide productivity growth. Productivity is a measure of how much

income is generated in an average hour of work in the economy. While

productivity after 1979 grew more slowly relative to previous decades,

it did grow steadily, offering the potential for broad-based wage gains.

But income gains were not broad-based. In fact, average pay (wages plus

benefits) for the 80 percent of the private-sector workers who are not

supervisors barely budged in that time. The growing wedge between

productivity and pay is the income generated by workers in the economy

that has been claimed by corporate owners and managers and others at the

very top of the pay scale.

{kind=link}

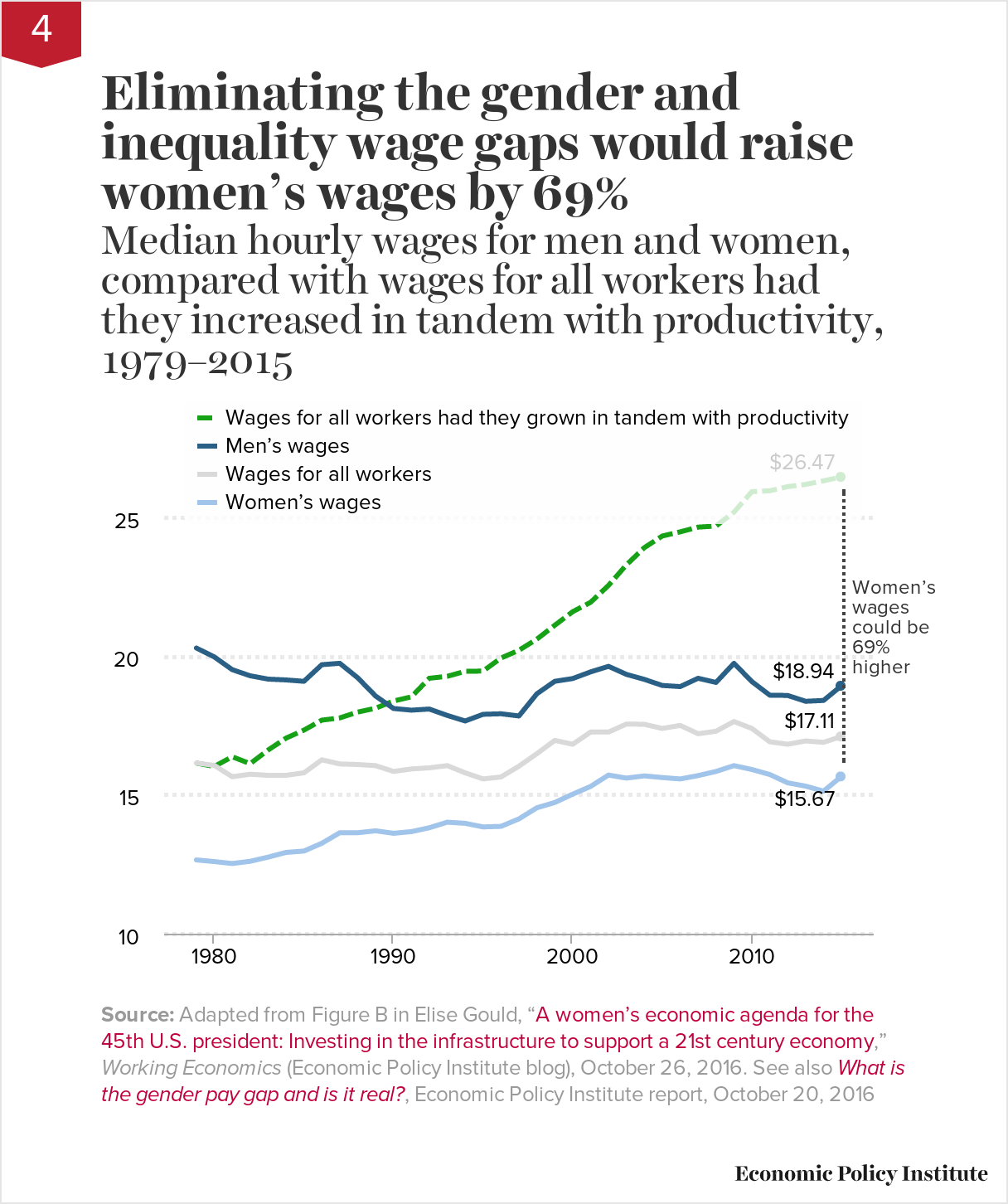

Eliminating the gender and inequality wage gaps would raise women’s wages by 69%Median hourly wages for men and women, compared with wages for all workers had they increased in tandem with productivity, 1979–2015

4

| Year | Wages for all workers | Men’s wages | Women’s wages | Wages for all workers had they grown in tandem with productivity |

|---|---|---|---|---|

| 1979 | $16.15 | $20.30 | $12.66 | $16.15 |

| 1980 | $16.07 | $19.98 | $12.60 | $16.03 |

| 1981 | $15.66 | $19.52 | $12.53 | $16.38 |

| 1982 | $15.75 | $19.30 | $12.61 | $16.13 |

| 1983 | $15.71 | $19.18 | $12.76 | $16.62 |

| 1984 | $15.71 | $19.15 | $12.93 | $17.05 |

| 1985 | $15.80 | $19.10 | $12.98 | $17.34 |

| 1986 | $16.27 | $19.70 | $13.26 | $17.70 |

| 1987 | $16.12 | $19.75 | $13.64 | $17.78 |

| 1988 | $16.10 | $19.23 | $13.64 | $17.99 |

| 1989 | $16.06 | $18.57 | $13.71 | $18.13 |

| 1990 | $15.85 | $18.12 | $13.62 | $18.39 |

| 1991 | $15.94 | $18.06 | $13.68 | $18.54 |

| 1992 | $15.98 | $18.10 | $13.82 | $19.21 |

| 1993 | $16.06 | $17.87 | $14.02 | $19.28 |

| 1994 | $15.80 | $17.67 | $13.98 | $19.46 |

| 1995 | $15.58 | $17.91 | $13.85 | $19.47 |

| 1996 | $15.65 | $17.93 | $13.87 | $19.94 |

| 1997 | $16.04 | $17.85 | $14.14 | $20.22 |

| 1998 | $16.49 | $18.65 | $14.54 | $20.62 |

| 1999 | $16.97 | $19.10 | $14.73 | $21.12 |

| 2000 | $16.83 | $19.20 | $15.03 | $21.61 |

| 2001 | $17.27 | $19.44 | $15.31 | $21.95 |

| 2002 | $17.27 | $19.64 | $15.72 | $22.56 |

| 2003 | $17.56 | $19.35 | $15.61 | $23.30 |

| 2004 | $17.55 | $19.17 | $15.69 | $23.92 |

| 2005 | $17.40 | $18.95 | $15.63 | $24.34 |

| 2006 | $17.51 | $18.91 | $15.58 | $24.49 |

| 2007 | $17.21 | $19.21 | $15.70 | $24.66 |

| 2008 | $17.30 | $19.06 | $15.85 | $24.70 |

| 2009 | $17.65 | $19.75 | $16.06 | $25.20 |

| 2010 | $17.40 | $19.09 | $15.92 | $25.94 |

| 2011 | $16.92 | $18.60 | $15.74 | $25.97 |

| 2012 | $16.83 | $18.59 | $15.44 | $26.12 |

| 2013 | $16.95 | $18.38 | $15.32 | $26.20 |

| 2014 | $16.90 | $18.41 | $15.14 | $26.33 |

| 2015 | 17.11 | 18.94 | 15.67 | 26.47 |

Women’s wages could be 69% higher

Source: Adapted from Figure B in Elise Gould, “A women’s economic agenda for the 45th U.S. president: Investing in the infrastructure to support a 21st century economy,” Working Economics (Economic Policy Institute blog), October 26, 2016. See also What is the gender pay gap and is it real?, Economic Policy Institute report, October 20, 2016

Closing the pay-productivity gap must be

a part of an agenda to improve women’s economic security. Although the

gap between what median men and median women are paid has narrowed

(albeit too slowly) since 1979, the gap between typical workers’

compensation and economy-wide productivity growth has widened. Tackling

both gaps would also raise the economic security of men. One example of

why the pay-productivity gap needs to inform our thinking about progress

in closing gender pay gaps is the fact that roughly a third of the

progress made in closing the median gender wage gap since 1979 was due

to the decline in men’s wages in an era of increasing inequality.

Remedying unfairness of pay for women is necessary, but wage parity

gained simply because male wages dropped is no cause for celebration.

The figure shows how high median wages for women could be if gender wage disparities had been closed between 1979 and today and if the economy had generated wage growth for all workers that matched economy-wide productivity growth. If the gender wage gap were closed and the economy’s gains broadly shared, women’s median hourly wages would be 69 percent higher today ($26.47 instead of $15.67). Notably, men’s median hourly wages would also be 40 percent higher. (To see how these differences compare for age and education cohorts, check out EPI’s new gender wage calculator.) These figures show that getting to gender pay equity is not a zero-sum game—if we also tackle inequality, typical men and women have much to gain.

The figure shows how high median wages for women could be if gender wage disparities had been closed between 1979 and today and if the economy had generated wage growth for all workers that matched economy-wide productivity growth. If the gender wage gap were closed and the economy’s gains broadly shared, women’s median hourly wages would be 69 percent higher today ($26.47 instead of $15.67). Notably, men’s median hourly wages would also be 40 percent higher. (To see how these differences compare for age and education cohorts, check out EPI’s new gender wage calculator.) These figures show that getting to gender pay equity is not a zero-sum game—if we also tackle inequality, typical men and women have much to gain.

{kind=link}

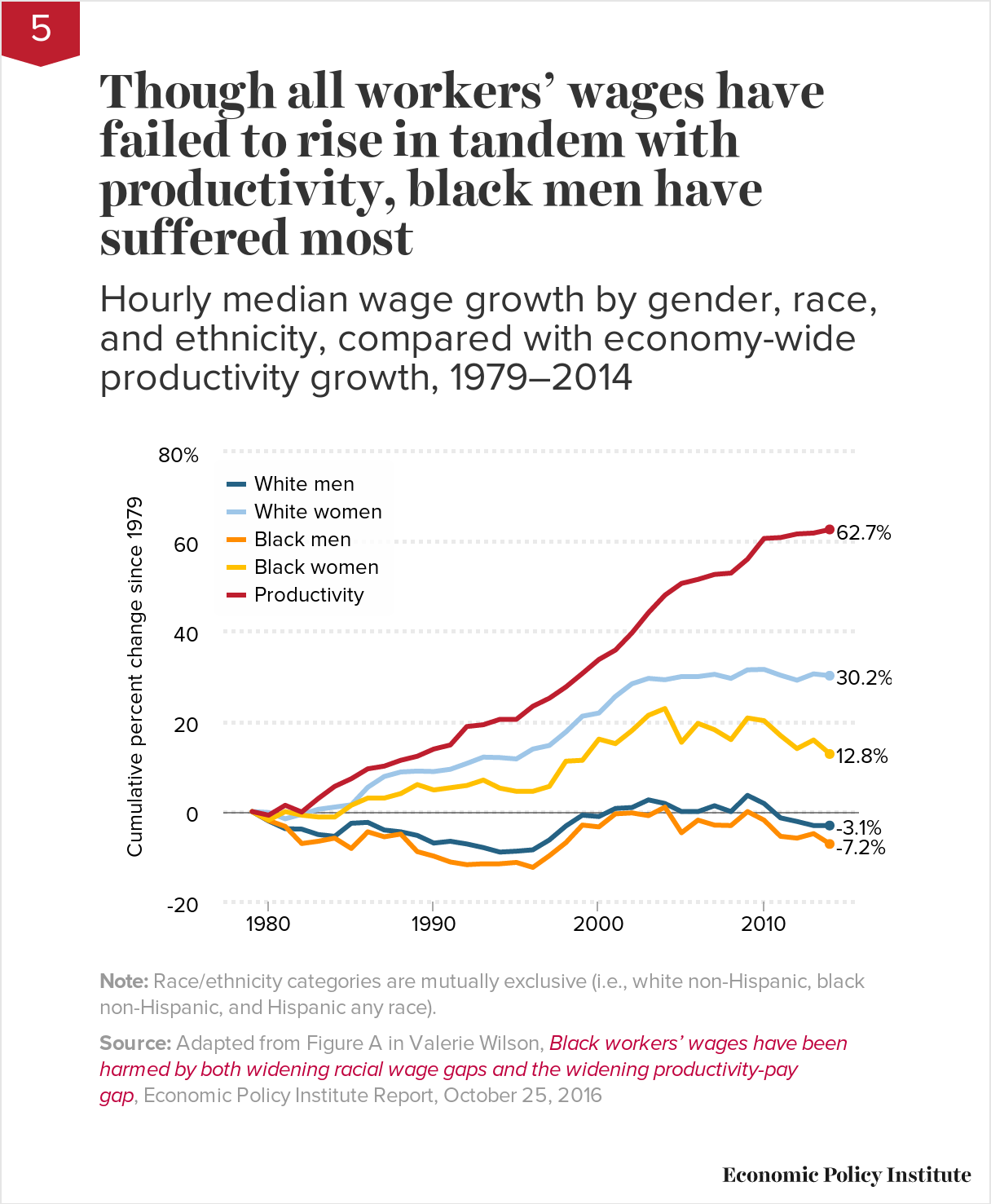

Though all workers’ wages have failed to rise in tandem with productivity, black men have suffered mostHourly median wage growth by gender, race, and ethnicity, compared with economy-wide productivity growth, 1979–2014

5

| Year | White men | White women | Black men | Black women | Productivity |

|---|---|---|---|---|---|

| 1979 | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% |

| 1980 | -2.1% | -0.2% | -2.0% | -1.9% | -0.8% |

| 1981 | -3.8% | -1.6% | -3.3% | 0.0% | 1.4% |

| 1982 | -3.9% | -0.6% | -7.1% | -0.8% | -0.1% |

| 1983 | -5.1% | 0.5% | -6.6% | -1.2% | 2.9% |

| 1984 | -5.5% | 1.0% | -5.9% | -1.2% | 5.6% |

| 1985 | -2.6% | 1.5% | -8.2% | 1.4% | 7.3% |

| 1986 | -2.4% | 5.4% | -4.5% | 3.0% | 9.5% |

| 1987 | -4.1% | 7.8% | -5.6% | 3.0% | 10.1% |

| 1988 | -4.5% | 8.8% | -5.0% | 4.0% | 11.4% |

| 1989 | -5.3% | 9.0% | -8.9% | 6.0% | 12.3% |

| 1990 | -7.0% | 8.9% | -9.9% | 4.8% | 13.9% |

| 1991 | -6.6% | 9.4% | -11.2% | 5.3% | 14.8% |

| 1992 | -7.2% | 10.7% | -11.8% | 5.8% | 18.9% |

| 1993 | -8.0% | 12.1% | -11.6% | 7.0% | 19.3% |

| 1994 | -9.0% | 12.0% | -11.6% | 5.2% | 20.5% |

| 1995 | -8.8% | 11.7% | -11.3% | 4.5% | 20.5% |

| 1996 | -8.5% | 13.9% | -12.4% | 4.5% | 23.4% |

| 1997 | -6.3% | 14.7% | -9.8% | 5.6% | 25.2% |

| 1998 | -3.2% | 17.7% | -6.9% | 11.2% | 27.7% |

| 1999 | -0.8% | 21.2% | -3.0% | 11.4% | 30.7% |

| 2000 | -1.1% | 21.9% | -3.4% | 16.1% | 33.8% |

| 2001 | 0.7% | 25.6% | -0.5% | 15.1% | 35.9% |

| 2002 | 0.9% | 28.4% | -0.3% | 18.0% | 39.7% |

| 2003 | 2.6% | 29.6% | -0.9% | 21.4% | 44.2% |

| 2004 | 1.8% | 29.3% | 1.0% | 22.9% | 48.1% |

| 2005 | 0.0% | 30.0% | -4.7% | 15.4% | 50.7% |

| 2006 | 0.0% | 30.0% | -1.9% | 19.6% | 51.6% |

| 2007 | 1.3% | 30.5% | -3.0% | 18.2% | 52.7% |

| 2008 | 0.0% | 29.6% | -3.1% | 16.0% | 53.0% |

| 2009 | 3.6% | 31.5% | 0.0% | 20.8% | 56.1% |

| 2010 | 1.8% | 31.6% | -1.9% | 20.2% | 60.7% |

| 2011 | -1.4% | 30.3% | -5.5% | 16.9% | 60.9% |

| 2012 | -2.2% | 29.2% | -5.9% | 14.0% | 61.7% |

| 2013 | -3.1% | 30.6% | -4.9% | 15.9% | 61.9% |

| 2014 | -3.1% | 30.2% | -7.2% | 12.8% | 62.7% |

Note: Race/ethnicity categories are mutually exclusive (i.e., white non-Hispanic, black non-Hispanic, and Hispanic any race).

Source: Adapted from Figure A in Valerie Wilson, Black workers’ wages have been harmed by both widening racial wage gaps and the widening productivity-pay gap, Economic Policy Institute Report, October 25, 2016

In the wake of Trump’s election, some

commentators have focused on the economic failures afflicting white

working-class men. White working-class men are suffering, but they are

not the only group suffering from the chasm between what the economy can

provide and what it is providing, and their loss has not translated

into gains made by typical workers of other races. In fact, wage gaps

between workers of different races have widened at the same time that

economy-wide productivity and wages for typical workers overall have

diverged. In short, what has caused sluggish wage growth for the vast

majority of all workers is the rise of inequality that has redistributed

income toward the very top of the income distribution.

The figure shows that between 1979 and 2015, median hourly real wage growth fell far short of productivity growth—a measure of the potential for pay increases—for men as well as for women and for both black and white workers. And white workers are not losing income to their black counterparts. Median hourly wages of black men fell 5.7 percent, compared with a 1.0 percent decline for white men. Median hourly wages of white women grew 31.6 percent, compared with 15.2 percent for black women.

What this figure does not show is that black workers already start out with a big pay disparity. In 2015, black workers overall were paid 26.2 percent less than their white peers. What has this double penalty of overall wage stagnation and regress on racial pay disparities cost black workers? Quite a lot, according to a 2016 report by Valerie Wilson. If the 1979 racial wage gap at the median had closed by 2015 and the overall median had grown with productivity (63.9 percent) between 1979 and 2015, the median black worker would be earning an hourly wage of $26.47 instead of $14.14—an increase of $12.33. That means the hourly wage of the median black worker would be an astounding 87.2 percent higher! And under this scenario, the median white worker would also receive an hourly pay increase of $7.30—the difference between $26.47 and $19.17—boosting their wages by 38.1 percent. The vast majority of workers of all races would be better off if we addressed both class and racial inequalities, with larger gains for African Americans because of the dual penalties imposed by class and race.

The figure shows that between 1979 and 2015, median hourly real wage growth fell far short of productivity growth—a measure of the potential for pay increases—for men as well as for women and for both black and white workers. And white workers are not losing income to their black counterparts. Median hourly wages of black men fell 5.7 percent, compared with a 1.0 percent decline for white men. Median hourly wages of white women grew 31.6 percent, compared with 15.2 percent for black women.

What this figure does not show is that black workers already start out with a big pay disparity. In 2015, black workers overall were paid 26.2 percent less than their white peers. What has this double penalty of overall wage stagnation and regress on racial pay disparities cost black workers? Quite a lot, according to a 2016 report by Valerie Wilson. If the 1979 racial wage gap at the median had closed by 2015 and the overall median had grown with productivity (63.9 percent) between 1979 and 2015, the median black worker would be earning an hourly wage of $26.47 instead of $14.14—an increase of $12.33. That means the hourly wage of the median black worker would be an astounding 87.2 percent higher! And under this scenario, the median white worker would also receive an hourly pay increase of $7.30—the difference between $26.47 and $19.17—boosting their wages by 38.1 percent. The vast majority of workers of all races would be better off if we addressed both class and racial inequalities, with larger gains for African Americans because of the dual penalties imposed by class and race.

{kind=link}

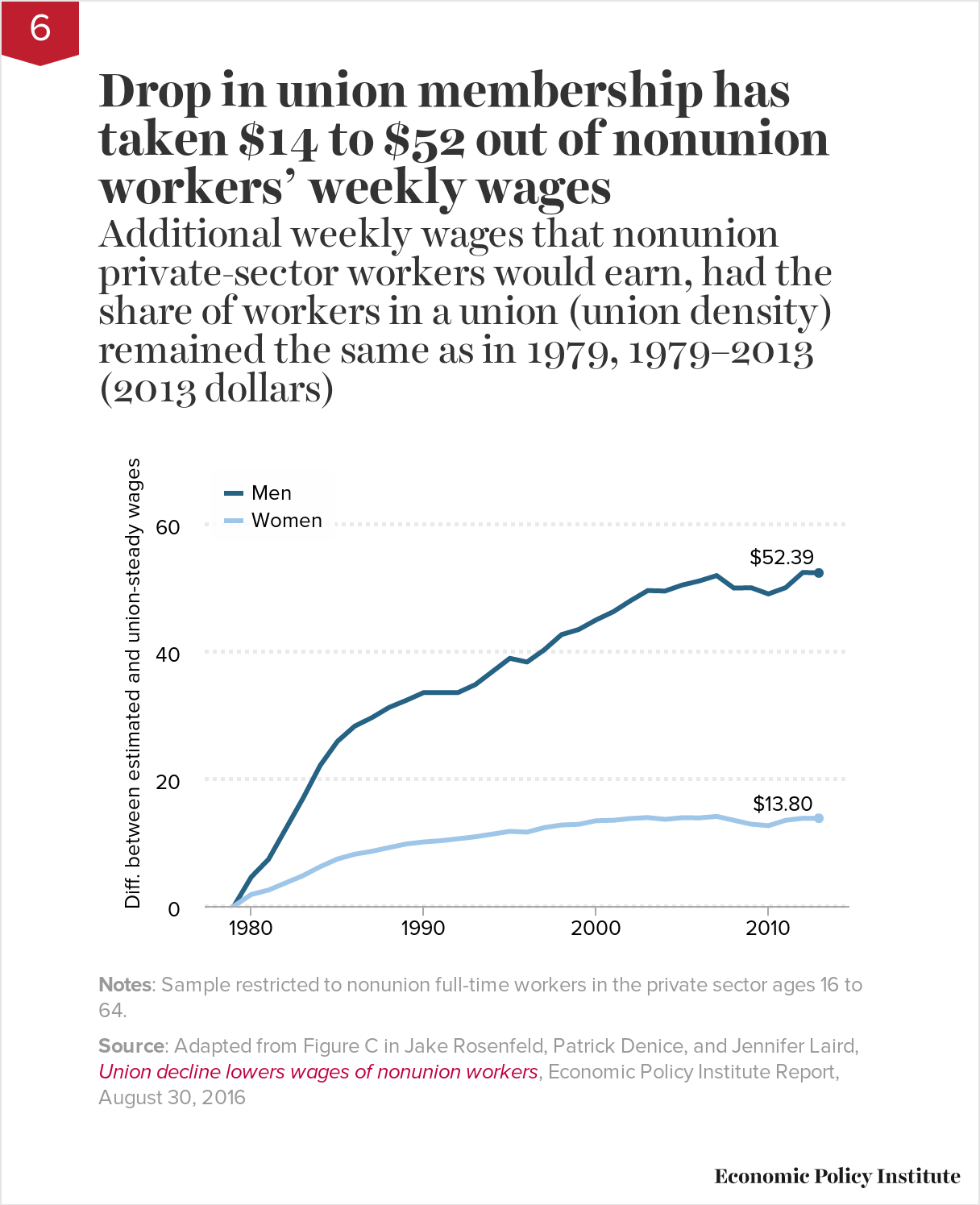

Drop in union membership has taken $14 to $52 out of nonunion workers’ weekly wagesAdditional weekly wages that nonunion private-sector workers would earn, had the share of workers in a union (union density) remained the same as in 1979, 1979–2013 (2013 dollars)

6

| Year | Men | Women |

|---|---|---|

| 1979 | 0.00 | 0.00 |

| 1980 | 4.55 | 1.81 |

| 1981 | 7.34 | 2.50 |

| 1983 | 16.93 | 4.77 |

| 1984 | 22.11 | 6.18 |

| 1985 | 25.90 | 7.39 |

| 1986 | 28.29 | 8.14 |

| 1987 | 29.63 | 8.60 |

| 1988 | 31.24 | 9.19 |

| 1989 | 32.36 | 9.76 |

| 1990 | 33.57 | 10.07 |

| 1991 | 33.57 | 10.27 |

| 1992 | 33.58 | 10.57 |

| 1993 | 34.83 | 10.89 |

| 1995 | 38.96 | 11.74 |

| 1996 | 38.38 | 11.62 |

| 1997 | 40.31 | 12.33 |

| 1998 | 42.69 | 12.74 |

| 1999 | 43.50 | 12.84 |

| 2000 | 45.00 | 13.41 |

| 2001 | 46.29 | 13.48 |

| 2002 | 48.02 | 13.76 |

| 2003 | 49.62 | 13.91 |

| 2004 | 49.55 | 13.63 |

| 2005 | 50.49 | 13.89 |

| 2006 | 51.14 | 13.86 |

| 2007 | 51.98 | 14.09 |

| 2008 | 50.01 | 13.48 |

| 2009 | 50.07 | 12.87 |

| 2010 | 49.09 | 12.63 |

| 2011 | 50.08 | 13.48 |

| 2012 | 52.48 | 13.80 |

| 2013 | $52.39 | $13.80 |

Notes: Sample restricted to nonunion full-time workers in the private sector ages 16 to 64.

Source: Adapted from Figure C in Jake Rosenfeld, Patrick Denice, and Jennifer Laird, Union decline lowers wages of nonunion workers, Economic Policy Institute Report, August 30, 2016

All workers would be better off in terms

of wage levels had the right of workers to associate and bargain

collectively not been severely eroded in recent decades. Between 1979

and 2013, the share of private-sector workers in a union fell from about

34 percent to 10 percent among men, and from 16 percent to 6 percent

among women. This decline in union density has eroded wages for nonunion

workers at every level of education and experience, costing billions in

lost wages. For the 32.9 million full-time nonunion women working in

the private sector and the 40.2 million full-time men working in the

private sector, there is a $133 billion loss in annual wages because of

weakened unions. This translates to real weekly wage losses for workers.

Women would be making $13.80 more a week and men would be making $52.39

more a week, had union density (the share of workers in similar

industries and regions who are union members) remained the same as in

1979.

Unions keep wages high for nonunion workers for several reasons. Union agreements set wage standards that nonunion employers follow. And a strong union presence prompts managers to keep wages high to prevent workers from organizing or leaving. Unions also set industry-wide norms, influencing what is seen as a “moral economy.”

Though not shown in the graph, working-class men have felt the decline in unionization the hardest. Specifically, nonunion men lacking a college degree would have earned 8 percent, or $3,016, more in 2013 if unions had remained as strong as they were in 1979.

Unions keep wages high for nonunion workers for several reasons. Union agreements set wage standards that nonunion employers follow. And a strong union presence prompts managers to keep wages high to prevent workers from organizing or leaving. Unions also set industry-wide norms, influencing what is seen as a “moral economy.”

Though not shown in the graph, working-class men have felt the decline in unionization the hardest. Specifically, nonunion men lacking a college degree would have earned 8 percent, or $3,016, more in 2013 if unions had remained as strong as they were in 1979.

{kind=link}

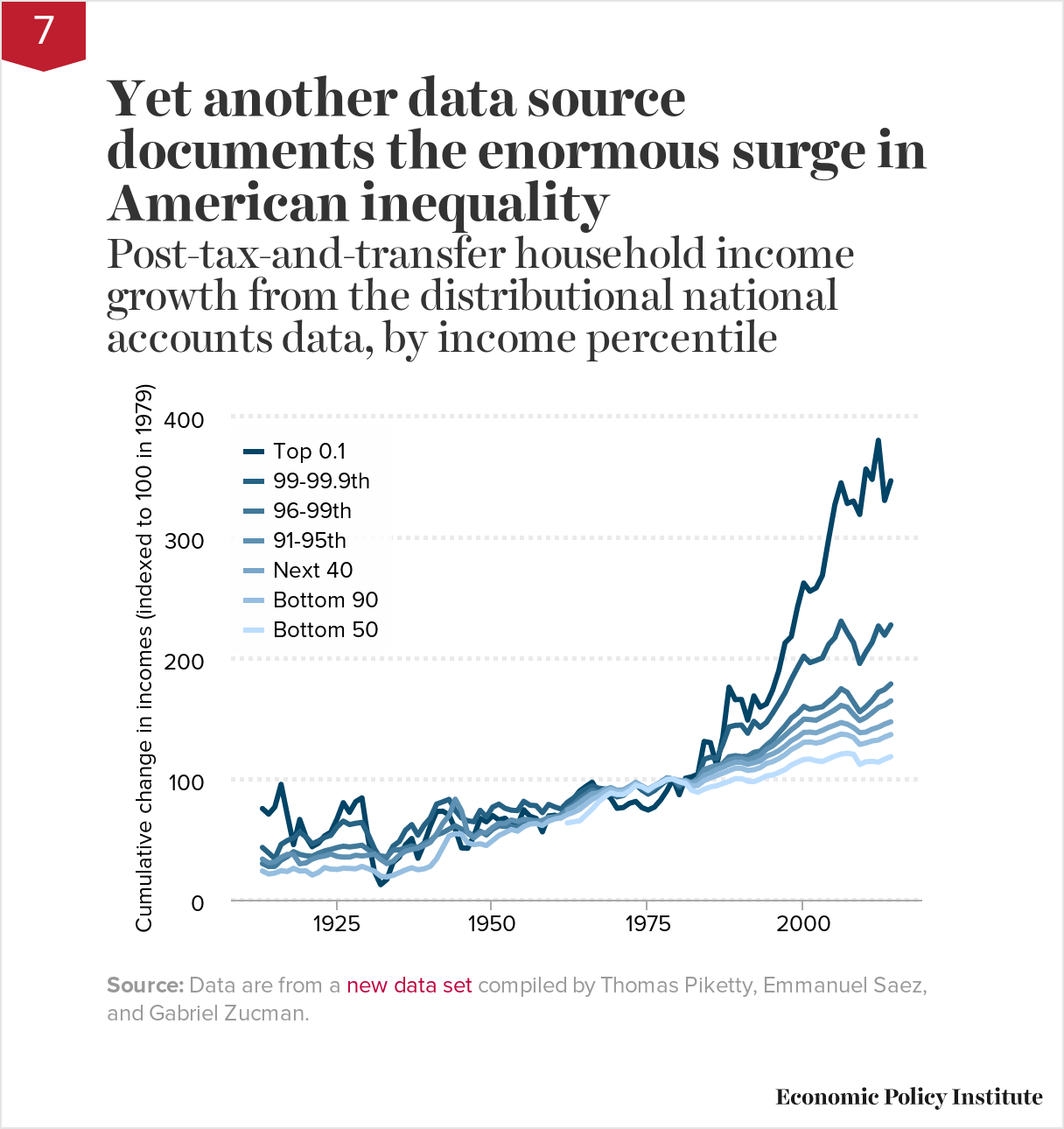

Yet another data source documents the enormous surge in American inequalityPost-tax-and-transfer household income growth from the distributional national accounts data, by income percentile

7

| Bottom 90 | Bottom 50 | Next 40 | 91-95th | 96-99th | 99-99.9th | Top 0.1 | |

|---|---|---|---|---|---|---|---|

| 1913 | 23.7327 | 33.65331 | 29.93943 | 43.27823 | 75.47623 | ||

| 1914 | 21.28975 | 30.44152 | 27.42943 | 38.72785 | 70.84473 | ||

| 1915 | 22.01303 | 31.29446 | 27.63197 | 33.98987 | 76.78276 | ||

| 1916 | 24.03428 | 35.05713 | 32.63794 | 45.75293 | 95.50515 | ||

| 1917 | 23.36389 | 37.55653 | 35.58478 | 48.98219 | 70.30063 | ||

| 1918 | 25.99977 | 37.45943 | 39.75538 | 51.13678 | 45.59054 | ||

| 1919 | 23.7557 | 29.73864 | 37.5025 | 55.97586 | 66.42215 | ||

| 1920 | 23.91308 | 30.49568 | 36.39877 | 52.00038 | 52.00913 | ||

| 1921 | 20.40423 | 33.57089 | 35.97857 | 46.24904 | 43.86804 | ||

| 1922 | 22.56271 | 35.35251 | 38.48873 | 48.60645 | 46.79869 | ||

| 1923 | 26.62762 | 36.18494 | 40.41201 | 51.57063 | 52.83884 | ||

| 1924 | 25.3325 | 37.78878 | 41.67534 | 53.30806 | 55.98231 | ||

| 1925 | 25.04011 | 35.89191 | 43.1564 | 60.36712 | 66.94126 | ||

| 1926 | 26.0494 | 35.2388 | 44.31057 | 65.07314 | 80.33322 | ||

| 1927 | 25.88253 | 35.26906 | 43.68758 | 62.20689 | 72.31164 | ||

| 1928 | 25.59061 | 36.8098 | 44.30285 | 63.26883 | 81.19631 | ||

| 1929 | 27.59766 | 36.22686 | 45.13929 | 63.97269 | 84.32806 | ||

| 1930 | 25.69753 | 36.78869 | 41.43329 | 53.91076 | 50.41799 | ||

| 1931 | 23.58497 | 37.6386 | 38.18021 | 42.38411 | 23.40733 | ||

| 1932 | 19.5378 | 33.37675 | 36.22934 | 33.874 | 12.42559 | ||

| 1933 | 18.8133 | 29.89834 | 35.59108 | 34.83715 | 16.7181 | ||

| 1934 | 20.12877 | 31.87053 | 41.05316 | 44.31979 | 30.83398 | ||

| 1935 | 22.40259 | 36.77853 | 41.38343 | 48.20434 | 35.22401 | ||

| 1936 | 24.67013 | 40.19861 | 42.85473 | 57.50882 | 45.48423 | ||

| 1937 | 26.43228 | 41.65951 | 44.5373 | 62.14962 | 50.66807 | ||

| 1938 | 24.79725 | 42.58223 | 43.10907 | 53.47296 | 34.3556 | ||

| 1939 | 25.55145 | 44.95177 | 46.81794 | 61.79799 | 46.51512 | ||

| 1940 | 27.62901 | 47.54603 | 48.92943 | 67.68232 | 61.10282 | ||

| 1941 | 33.88191 | 54.39828 | 53.65169 | 79.19836 | 73.09964 | ||

| 1942 | 43.29914 | 63.3563 | 55.50446 | 81.06559 | 73.31078 | ||

| 1943 | 52.80965 | 69.71679 | 58.40494 | 83.07906 | 70.12778 | ||

| 1944 | 54.60111 | 83.20119 | 61.25023 | 73.92529 | 58.40418 | ||

| 1945 | 54.2032 | 73.59434 | 58.5029 | 67.72197 | 42.88401 | ||

| 1946 | 47.1023 | 54.98784 | 55.75051 | 65.37271 | 42.55941 | ||

| 1947 | 45.61777 | 51.27523 | 52.65075 | 64.54918 | 52.81662 | ||

| 1948 | 46.27771 | 55.32878 | 56.69584 | 73.94818 | 67.30207 | ||

| 1949 | 44.85111 | 55.47728 | 53.61912 | 68.53701 | 64.51888 | ||

| 1950 | 48.95762 | 59.82028 | 58.26081 | 76.67206 | 69.6535 | ||

| 1951 | 53.13092 | 63.30267 | 61.1851 | 79.11648 | 66.05985 | ||

| 1952 | 55.543 | 63.20365 | 60.6588 | 75.66076 | 67.4788 | ||

| 1953 | 58.13027 | 66.00397 | 60.82156 | 74.12246 | 62.29707 | ||

| 1954 | 56.74598 | 64.72895 | 59.72348 | 73.76929 | 61.18403 | ||

| 1955 | 60.45715 | 66.59386 | 64.45841 | 81.47777 | 74.45941 | ||

| 1956 | 62.6146 | 66.07277 | 65.53554 | 78.24851 | 69.06196 | ||

| 1957 | 63.07287 | 64.54181 | 65.75526 | 77.86183 | 67.29979 | ||

| 1958 | 61.44245 | 65.657 | 65.02915 | 72.07397 | 56.18065 | ||

| 1959 | 65.02998 | 68.06952 | 68.14701 | 78.90449 | 69.33398 | ||

| 1960 | 66.89607 | 68.68847 | 68.1266 | 76.77248 | 69.91774 | ||

| 1961 | 67.78351 | 69.65426 | 70.63115 | 75.09075 | 67.87351 | ||

| 1962 | 70.4927 | 63.64325 | 74.46108 | 73.76656 | 75.63827 | 80.53871 | 77.82573 |

| 1963 | 72.34403 | 64.45871 | 76.91257 | 77.00796 | 79.27725 | 84.17178 | 83.4488 |

| 1964 | 74.78534 | 65.27417 | 80.29585 | 80.97379 | 83.68492 | 88.60585 | 90.01243 |

| 1965 | 78.97684 | 70.13567 | 84.09917 | 84.71663 | 87.38434 | 91.63466 | 93.81867 |

| 1966 | 83.00219 | 74.99717 | 87.64008 | 88.19319 | 90.8142 | 94.28764 | 97.31097 |

| 1967 | 85.64931 | 80.78541 | 88.46732 | 87.65472 | 88.85984 | 92.36706 | 88.88887 |

| 1968 | 89.01593 | 85.16668 | 91.24607 | 89.55186 | 89.20251 | 91.6852 | 88.51358 |

| 1969 | 91.25928 | 88.4355 | 92.8953 | 90.5163 | 88.4021 | 88.0171 | 83.84223 |

| 1970 | 89.31669 | 87.15028 | 90.57185 | 88.66994 | 86.42245 | 85.17894 | 75.69672 |

| 1971 | 89.55088 | 87.09922 | 90.9713 | 89.31088 | 87.57022 | 86.35819 | 76.34119 |

| 1972 | 92.38655 | 90.03742 | 93.74757 | 92.96691 | 92.13266 | 90.75359 | 79.82626 |

| 1973 | 96.11671 | 94.64942 | 96.96682 | 96.91853 | 96.75554 | 95.51017 | 81.34194 |

| 1974 | 94.02037 | 93.52424 | 94.30781 | 93.87008 | 92.52697 | 90.70497 | 76.23273 |

| 1975 | 91.01398 | 90.52585 | 91.29679 | 90.96083 | 89.50955 | 87.40869 | 74.26816 |

| 1976 | 94.35718 | 94.2051 | 94.44529 | 94.31208 | 92.73313 | 90.32411 | 76.67994 |

| 1977 | 96.81916 | 96.52656 | 96.98868 | 97.28635 | 96.48129 | 94.6759 | 82.49974 |

| 1978 | 99.88037 | 99.34863 | 100.1884 | 100.8638 | 100.2407 | 98.91114 | 90.22779 |

| 1979 | 100 | 100 | 100 | 100 | 100 | 100 | 100 |

| 1980 | 98.26488 | 97.61414 | 98.64191 | 97.76216 | 94.80523 | 93.1143 | 86.91483 |

| 1981 | 97.68509 | 96.23014 | 98.52805 | 98.91017 | 97.19851 | 98.64778 | 100.612 |

| 1982 | 94.07145 | 90.60212 | 96.08148 | 96.72842 | 94.56753 | 95.22981 | 101.7506 |

| 1983 | 94.64854 | 88.9539 | 97.94785 | 100.3394 | 97.77981 | 101.0831 | 103.9856 |

| 1984 | 98.68139 | 91.5108 | 102.8358 | 107.8385 | 107.5276 | 116.219 | 131.004 |

| 1985 | 100.8055 | 93.33651 | 105.1329 | 109.655 | 108.4626 | 118.0252 | 130.057 |

| 1986 | 102.7875 | 94.35348 | 107.6739 | 111.2332 | 109.3253 | 116.9127 | 110.9831 |

| 1987 | 104.7421 | 96.2283 | 109.6748 | 111.9271 | 112.8364 | 128.7529 | 134.6872 |

| 1988 | 106.8402 | 97.96563 | 111.982 | 115.4286 | 118.3864 | 143.0172 | 175.9767 |

| 1989 | 108.8137 | 100.2283 | 113.7879 | 116.895 | 119.2596 | 144.3395 | 165.6537 |

| 1990 | 108.8275 | 100.2639 | 113.789 | 116.7634 | 118.5356 | 144.6014 | 165.7722 |

| 1991 | 106.9756 | 98.14099 | 112.0942 | 115.7375 | 118.7417 | 137.8344 | 148.6849 |

| 1992 | 107.6168 | 97.72335 | 113.3488 | 117.3251 | 122.0337 | 147.7052 | 168.7361 |

| 1993 | 109.3271 | 99.80908 | 114.8416 | 119.6654 | 123.0398 | 142.693 | 159.3989 |

| 1994 | 112.7897 | 102.5032 | 118.7495 | 124.494 | 127.9362 | 146.7308 | 162.0879 |

| 1995 | 114.2954 | 103.2037 | 120.7217 | 127.2814 | 132.2493 | 154.3844 | 173.5347 |

| 1996 | 116.8251 | 105.3766 | 123.458 | 131.5369 | 138.125 | 162.6432 | 189.7594 |

| 1997 | 120.0619 | 107.7359 | 127.2032 | 136.0553 | 143.8332 | 171.3382 | 212.6514 |

| 1998 | 124.279 | 111.47 | 131.7001 | 140.7231 | 150.4667 | 182.4624 | 217.8013 |

| 1999 | 127.0094 | 113.8701 | 134.6219 | 144.6325 | 154.4141 | 192.1739 | 242.2452 |

| 2000 | 130.2871 | 116.1185 | 138.496 | 149.5242 | 160.0374 | 201.6449 | 262.2195 |

| 2001 | 130.563 | 116.4413 | 138.7448 | 149.1107 | 157.6435 | 196.2731 | 255.3759 |

| 2002 | 129.6873 | 115.0149 | 138.188 | 148.5807 | 158.6449 | 198.1229 | 258.2305 |

| 2003 | 130.7376 | 114.3935 | 140.2069 | 151.4572 | 159.7162 | 200.1824 | 268.4298 |

| 2004 | 133.1071 | 116.6533 | 142.6401 | 154.2173 | 164.2175 | 211.3237 | 298.3971 |

| 2005 | 135.1675 | 118.907 | 144.5884 | 157.2676 | 168.406 | 216.9945 | 327.02 |

| 2006 | 137.0963 | 120.5917 | 146.6586 | 160.8505 | 174.6956 | 230.622 | 345.1448 |

| 2007 | 136.5364 | 121.2232 | 145.4084 | 159.4222 | 171.626 | 221.0781 | 328.095 |

| 2008 | 134.4407 | 120.4954 | 142.5202 | 153.4786 | 163.4876 | 212.8995 | 330.0312 |

| 2009 | 128.613 | 111.9696 | 138.2557 | 148.2443 | 155.5828 | 195.6494 | 318.9889 |

| 2010 | 129.7716 | 114.2373 | 138.7717 | 150.9138 | 159.7115 | 205.1275 | 356.6267 |

| 2011 | 131.4316 | 114.5713 | 141.2 | 154.8323 | 165.0593 | 213.0578 | 348.0072 |

| 2012 | 132.2085 | 113.8685 | 142.8342 | 159.1319 | 171.7283 | 226.6272 | 380.3506 |

| 2013 | 134.7136 | 116.3695 | 145.3417 | 161.0668 | 174.0647 | 219.045 | 330.5724 |

| 2014 | 136.7039 | 118.4258 | 147.2938 | 164.6328 | 178.6594 | 227.4947 | 346.8308 |

Source: Data are from a new data set compiled by Thomas Piketty, Emmanuel Saez, and Gabriel Zucman.

A new data set confirms what we know

about the enormous increase in income inequality after 1979. This data

set allows us to take another cut at this issue, with all of total

national income and its distribution accounted for—market-based incomes

like wages and dividends, transfer incomes like Social Security and

Medicare, and even the income stemming from direct government purchases.

The figure charts incomes (indexed to be 100 in 1979) for the bottom 50

percent of households, bottom 90 percent of households, households

between the 50th and 90th percentiles, households in subgroups of the

top 10 percent, and the top 0.1 percent of households. The results are

clear: households nearer the top of the income distribution have seen

far more rapid growth in recent decades. And counting income in the form

of government benefits does not close the gap between income growth at

the top and the income growth of everybody else.

{kind=link}

The gap between the retirement ‘haves’ and ‘have-nots’ has grown since the recessionRetirement account savings of families age 32–61 by savings percentile, 1989–2013 (2013 dollars)

8

| 50th (median) | 60th | 70th | 80th | 90th | |

|---|---|---|---|---|---|

| 1989 | $0 | $5,423 | $14,461 | $32,536 | $90,379 |

| 1992 | $0 | $4,874 | $16,248 | $39,384 | $90,987 |

| 1995 | $2,277 | $9,866 | $24,286 | $47,054 | $113,841 |

| 1998 | $6,004 | $17,440 | $38,597 | $73,763 | $160,106 |

| 2001 | $7,879 | $23,638 | $48,326 | $92,818 | $223,247 |

| 2004 | $6,166 | $19,730 | $49,326 | $102,351 | $246,628 |

| 2007 | $11,228 | $30,315 | $61,754 | $123,508 | $258,243 |

| 2010 | $5,358 | $19,291 | $42,868 | $96,453 | $246,490 |

| 2013 | $5,000 | $20,100 | $50,000 | $116,000 | $274,000 |

Note: Retirement account savings include 401(k)s, IRAs, and Keogh plans. Scale changed to accommodate larger values.

Source: Adapted from Figure 9 in Monique Morrissey, The State of American Retirement:

How 401(k)s have failed most American workers, Economic Policy Institute Report, March 3, 2016

How 401(k)s have failed most American workers, Economic Policy Institute Report, March 3, 2016

Over the past generation of economic

life, the U.S. economy undertook a grand experiment in making

defined-contribution (DC) pension plans such as 401(k)s, often financed

directly by workers’ savings themselves, the primary vehicle of private

retirement security. This experiment has decisively failed. Overall

pension coverage has not increased, and fewer Americans are in

defined-benefit (DB) plans (think company pensions). The DB plans

crowded out by DC plans were more secure, providing a guaranteed income

for life that was not subject to the vagaries of the stock market. They

were also much more equal than DC plans because they were

employer-funded and participation was automatic (rather than workers

bearing most of the costs and all of the risks).

Nearly half of working-age families have nothing saved in retirement accounts, and the median working-age family had only $5,000 saved in 2013. Meanwhile, families in the 90th percentile of retirement savings had $274,000 in retirement, and the top 1 percent of families had $1,080,000 or more (not shown on chart). These huge disparities reflect a growing gap between the haves and the have-nots since the Great Recession, as accounts with smaller balances have stagnated while larger ones have rebounded.

Nearly half of working-age families have nothing saved in retirement accounts, and the median working-age family had only $5,000 saved in 2013. Meanwhile, families in the 90th percentile of retirement savings had $274,000 in retirement, and the top 1 percent of families had $1,080,000 or more (not shown on chart). These huge disparities reflect a growing gap between the haves and the have-nots since the Great Recession, as accounts with smaller balances have stagnated while larger ones have rebounded.

{kind=link}

Fiscal austerity explains why recovery has been so long in comingChange in per capita government spending during recoveries of the last four recessions

9

| 1982Q4 | 1991Q1 | 2001Q4 | 2009Q2 | |

|---|---|---|---|---|

| -6 | 90.83817 | |||

| -5 | 96.46779 | 91.33168 | ||

| -4 | 96.72548 | 97.80345 | ||

| -3 | 96.51523 | 96.35624 | 94.05089 | |

| -2 | 97.21731 | 98.09825 | 98.14218 | 94.4813 |

| -1 | 98.26435 | 98.92533 | 97.98324 | 96.68474 |

| 0 | 100 | 100 | 100 | 100 |

| 1 | 100.3829 | 100.7468 | 101.5275 | 99.84022 |

| 2 | 100.9558 | 100.4456 | 102.3723 | 99.50632 |

| 3 | 101.005 | 100.9653 | 102.8023 | 100.7222 |

| 4 | 99.79553 | 102.3054 | 103.3013 | 101.0192 |

| 5 | 100.4771 | 102.4831 | 103.1351 | 101.1242 |

| 6 | 101.715 | 102.7714 | 104.3665 | 100.3432 |

| 7 | 102.037 | 102.2554 | 104.5556 | 98.88213 |

| 8 | 103.485 | 101.9195 | 104.6451 | 98.15822 |

| 9 | 104.602 | 101.724 | 105.4192 | 97.23836 |

| 10 | 106.0107 | 102.011 | 105.8382 | 96.86414 |

| 11 | 107.6073 | 101.868 | 105.804 | 95.9267 |

| 12 | 107.6288 | 101.2959 | 105.4445 | 95.78736 |

| 13 | 108.7749 | 101.4328 | 106.1767 | 95.40735 |

| 14 | 110.4932 | 102.1325 | 106.3521 | 94.83589 |

| 15 | 112.3029 | 101.9209 | 106.5289 | 94.21625 |

| 16 | 111.6476 | 102.6275 | 106.0185 | 93.90439 |

| 17 | 112.0741 | 102.8173 | 107.5423 | 93.62299 |

| 18 | 112.6221 | 102.3836 | 107.6773 | 93.04895 |

| 19 | 112.3952 | 101.1486 | 107.8776 | 93.22292 |

| 20 | 113.0807 | 101.9359 | 108.2144 | 93.60604 |

| 21 | 113.3476 | 103.2437 | 109.1187 | 94.245 |

| 22 | 113.3408 | 102.7047 | 109.0787 | 94.14226 |

| 23 | 113.108 | 102.7598 | 109.5846 | 95.09063 |

| 24 | 114.405 | 103.1194 | 109.8789 | 95.43504 |

| 25 | 114.9973 | 103.4402 | 95.722 | |

| 26 | 116.1049 | 103.3562 | 95.86387 | |

| 27 | 116.8758 | 103.2392 | 96.35498 |

Note:

For total government spending, government consumption and investment

expenditures are deflated with the NIPA price deflator. Government

transfer payments are deflated with the price deflator for personal

consumption expenditures. This figure includes state and local

government spending.

Source: Adapted from Figure B in Josh Bivens, Why is recovery taking so long—and who’s to blame?, Economic Policy Institute Report, August 11, 2016

The agonizingly slow

pace of recovery from the Great Recession is easy to explain: it is the

result of austerity policies championed by Republican policymakers at

the federal and state levels. Like every other postwar recession before

it, the Great Recession was caused by a shortfall in aggregate demand,

meaning that the spending of households, businesses, and governments was

not sufficient to keep the economy’s resources fully employed.

Despite the Great Recession being the sharpest and longest on record

since World War II, and despite monetary policy reaching its

conventional limits to boost spending early in the recession,

policymakers made damaging decisions to limit public spending following

the recession’s trough in 2009. This growth has been historically slow

relative to other business cycles even as the economy needed

substantially faster-than-average growth to mount a full and timely

recovery.

The figure shows the growth in per capita spending

by federal, state, and local governments following the troughs of the

four recessions. Astoundingly, per capita government spending in the

first quarter of 2016—27 quarters into the recovery—was nearly 3.5

percent lower than it was at the trough of the Great Recession. By

contrast, 27 quarters into the early 1990s recovery, per capita

government spending was 3 percent higher than at the trough; 23 quarters

following the early 2000s recession (a shorter recovery), it was 10

percent higher; and 27 quarters into the early 1980s recovery, it was 17

percent higher.

{kind=link}

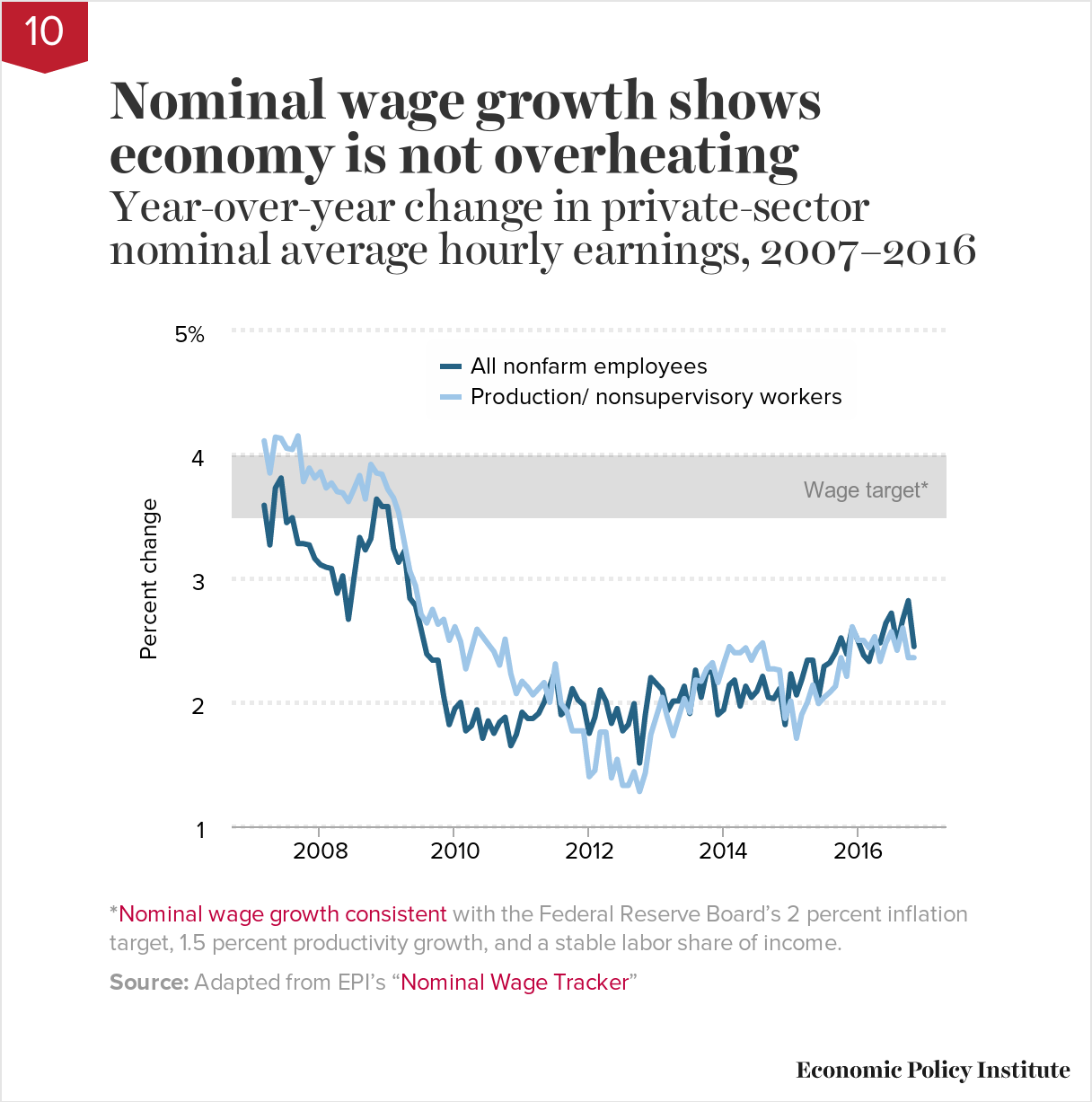

Nominal wage growth shows economy is not overheatingYear-over-year change in private-sector nominal average hourly earnings, 2007–2016

10

| All nonfarm employees | Production/nonsupervisory workers | |

|---|---|---|

| Mar-2007 | 3.59% | 4.11% |

| Apr-2007 | 3.27% | 3.85% |

| May-2007 | 3.73% | 4.14% |

| Jun-2007 | 3.81% | 4.13% |

| Jul-2007 | 3.45% | 4.05% |

| Aug-2007 | 3.49% | 4.04% |

| Sep-2007 | 3.28% | 4.15% |

| Oct-2007 | 3.28% | 3.78% |

| Nov-2007 | 3.27% | 3.89% |

| Dec-2007 | 3.16% | 3.81% |

| Jan-2008 | 3.11% | 3.86% |

| Feb-2008 | 3.09% | 3.73% |

| Mar-2008 | 3.08% | 3.77% |

| Apr-2008 | 2.88% | 3.70% |

| May-2008 | 3.02% | 3.69% |

| Jun-2008 | 2.67% | 3.62% |

| Jul-2008 | 3.00% | 3.72% |

| Aug-2008 | 3.33% | 3.83% |

| Sep-2008 | 3.23% | 3.64% |

| Oct-2008 | 3.32% | 3.92% |

| Nov-2008 | 3.64% | 3.85% |

| Dec-2008 | 3.58% | 3.84% |

| Jan-2009 | 3.58% | 3.72% |

| Feb-2009 | 3.24% | 3.65% |

| Mar-2009 | 3.13% | 3.53% |

| Apr-2009 | 3.22% | 3.29% |

| May-2009 | 2.84% | 3.06% |

| Jun-2009 | 2.78% | 2.94% |

| Jul-2009 | 2.59% | 2.71% |

| Aug-2009 | 2.39% | 2.64% |

| Sep-2009 | 2.34% | 2.75% |

| Oct-2009 | 2.34% | 2.63% |

| Nov-2009 | 2.05% | 2.67% |

| Dec-2009 | 1.82% | 2.50% |

| Jan-2010 | 1.95% | 2.61% |

| Feb-2010 | 2.00% | 2.49% |

| Mar-2010 | 1.77% | 2.27% |

| Apr-2010 | 1.81% | 2.43% |

| May-2010 | 1.94% | 2.59% |

| Jun-2010 | 1.71% | 2.53% |

| Jul-2010 | 1.85% | 2.47% |

| Aug-2010 | 1.75% | 2.41% |

| Sep-2010 | 1.84% | 2.30% |

| Oct-2010 | 1.88% | 2.51% |

| Nov-2010 | 1.65% | 2.23% |

| Dec-2010 | 1.74% | 2.07% |

| Jan-2011 | 1.92% | 2.17% |

| Feb-2011 | 1.87% | 2.12% |

| Mar-2011 | 1.87% | 2.06% |

| Apr-2011 | 1.91% | 2.11% |

| May-2011 | 2.00% | 2.16% |

| Jun-2011 | 2.13% | 2.00% |

| Jul-2011 | 2.26% | 2.31% |

| Aug-2011 | 1.90% | 1.99% |

| Sep-2011 | 1.94% | 1.93% |

| Oct-2011 | 2.11% | 1.77% |

| Nov-2011 | 2.02% | 1.77% |

| Dec-2011 | 1.98% | 1.77% |

| Jan-2012 | 1.75% | 1.40% |

| Feb-2012 | 1.88% | 1.45% |

| Mar-2012 | 2.10% | 1.76% |

| Apr-2012 | 2.01% | 1.76% |

| May-2012 | 1.83% | 1.39% |

| Jun-2012 | 1.95% | 1.54% |

| Jul-2012 | 1.77% | 1.33% |

| Aug-2012 | 1.82% | 1.33% |

| Sep-2012 | 1.99% | 1.44% |

| Oct-2012 | 1.51% | 1.28% |

| Nov-2012 | 1.90% | 1.43% |

| Dec-2012 | 2.20% | 1.74% |

| Jan-2013 | 2.15% | 1.89% |

| Feb-2013 | 2.10% | 2.04% |

| Mar-2013 | 1.93% | 1.88% |

| Apr-2013 | 2.01% | 1.73% |

| May-2013 | 2.01% | 1.88% |

| Jun-2013 | 2.13% | 2.03% |

| Jul-2013 | 1.91% | 1.92% |

| Aug-2013 | 2.26% | 2.18% |

| Sep-2013 | 2.04% | 2.17% |

| Oct-2013 | 2.25% | 2.27% |

| Nov-2013 | 2.24% | 2.32% |

| Dec-2013 | 1.90% | 2.16% |

| Jan-2014 | 1.94% | 2.31% |

| Feb-2014 | 2.14% | 2.45% |

| Mar-2014 | 2.18% | 2.40% |

| Apr-2014 | 1.97% | 2.40% |

| May-2014 | 2.13% | 2.44% |

| Jun-2014 | 2.04% | 2.34% |

| Jul-2014 | 2.09% | 2.43% |

| Aug-2014 | 2.21% | 2.48% |

| Sep-2014 | 2.04% | 2.27% |

| Oct-2014 | 2.03% | 2.27% |

| Nov-2014 | 2.11% | 2.26% |

| Dec-2014 | 1.82% | 1.87% |

| Jan-2015 | 2.23% | 2.01% |

| Feb-2015 | 2.06% | 1.71% |

| Mar-2015 | 2.18% | 1.90% |

| Apr-2015 | 2.34% | 2.00% |

| May-2015 | 2.34% | 2.14% |

| Jun-2015 | 2.04% | 1.99% |

| Jul-2015 | 2.29% | 2.04% |

| Aug-2015 | 2.32% | 2.08% |

| Sep-2015 | 2.40% | 2.13% |

| Oct-2015 | 2.52% | 2.36% |

| Nov-2015 | 2.39% | 2.21% |

| Dec-2015 | 2.60% | 2.61% |

| Jan-2016 | 2.50% | 2.50% |

| Feb-2016 | 2.38% | 2.50% |

| Mar-2016 | 2.33% | 2.44% |

| Apr-2016 | 2.49% | 2.53% |

| May-2016 | 2.48% | 2.33% |

| Jun-2016 | 2.64% | 2.48% |

| Jul-2016 | 2.72% | 2.57% |

| Aug-2016 | 2.47% | 2.42% |

| Sep-2016 | 2.67% | 2.60% |

| Oct-2016 | 2.82% | 2.36% |

| Nov-2016 | 2.45% | 2.36% |

*Nominal wage growth consistent

with the Federal Reserve Board’s 2 percent inflation target,

1.5 percent productivity growth, and a stable labor share of income.

Source: Adapted from EPI’s “Nominal Wage Tracker”

The year 2017 looks to be the year that the Fed begins raising short-term interest rates in earnest. The Fed should raise

rates only when it fears the economy is growing too fast and pushing

unemployment low enough that workers are empowered to demand (and get)

raises above what their productivity justifies. Data on nominal wage

growth show that the economy is not getting overheated and thus a rate

increase is not justified.

The pace of economic growth should be considered unsustainable only when increases in labor costs force firms to raise prices enough to accelerate inflation above the Federal Reserve’s stated goal of 2 percent inflation. An absolutely crucial link in this chain is wage growth. If nominal (i.e., not inflation-adjusted) wages simply grow at the rate of economy-wide productivity, then wages are putting no upward pressure on prices. To see why, think of a 2 percent raise in hourly pay of a worker whose productivity (how much they produce in an hour) also rises 2 percent. The worker is getting 2 percent more, but is also producing 2 percent more. So the labor cost per unit of output is unchanged, and there is zero upward pressure on firms’ costs, or overall inflation. And the goal of Federal Reserve policy is not zero upward pressure on prices (or 0 percent inflation). Their stated target is 2 percent inflation. This means that nominal wages can grow at the rate of economy-wide productivity growth plus 2 percent before they are putting enough upward pressure on prices to make the Fed rein them in. EPI’s nominal wage tracker looks are how wages have grown over this recovery relative to a target of 1.5 percent (a common estimate of long-run, trend productivity growth) plus 2 percent. Nominal wage growth has been consistently below this target, meaning there is very little reason to worry about overheating in the economy.

The pace of economic growth should be considered unsustainable only when increases in labor costs force firms to raise prices enough to accelerate inflation above the Federal Reserve’s stated goal of 2 percent inflation. An absolutely crucial link in this chain is wage growth. If nominal (i.e., not inflation-adjusted) wages simply grow at the rate of economy-wide productivity, then wages are putting no upward pressure on prices. To see why, think of a 2 percent raise in hourly pay of a worker whose productivity (how much they produce in an hour) also rises 2 percent. The worker is getting 2 percent more, but is also producing 2 percent more. So the labor cost per unit of output is unchanged, and there is zero upward pressure on firms’ costs, or overall inflation. And the goal of Federal Reserve policy is not zero upward pressure on prices (or 0 percent inflation). Their stated target is 2 percent inflation. This means that nominal wages can grow at the rate of economy-wide productivity growth plus 2 percent before they are putting enough upward pressure on prices to make the Fed rein them in. EPI’s nominal wage tracker looks are how wages have grown over this recovery relative to a target of 1.5 percent (a common estimate of long-run, trend productivity growth) plus 2 percent. Nominal wage growth has been consistently below this target, meaning there is very little reason to worry about overheating in the economy.

{kind=link}

The U.S. has a lower share of prime-age women with a job than do peer countriesEmployment-to-population ratio of women workers age 25–54, select countries, 1995–2014

11

| Canada | Germany | Japan | United States | |

|---|---|---|---|---|

| 1995 | 69.434551% | 66.360158% | 63.233624% | 72.189196% |

| 1996 | 69.577146% | 67.220440% | 63.701741% | 72.770073% |

| 1997 | 70.971110% | 67.399584% | 64.566038% | 73.541046% |

| 1998 | 72.183646% | 68.944387% | 64.036077% | 73.642970% |

| 1999 | 73.245982% | 70.253128% | 63.551051% | 74.147991% |

| 2000 | 73.944309% | 71.210539% | 63.582090% | 74.213847% |

| 2001 | 74.297867% | 71.607431% | 64.124398% | 73.421299% |

| 2002 | 75.348504% | 71.845950% | 63.863976% | 72.259684% |

| 2003 | 76.000458% | 71.981067% | 64.407421% | 72.006189% |

| 2004 | 76.720415% | 72.129055% | 65.028791% | 71.848458% |

| 2005 | 76.488663% | 70.969949% | 65.733178% | 71.963537% |

| 2006 | 76.984912% | 72.647765% | 66.614235% | 72.504467% |

| 2007 | 78.190906% | 74.045933% | 67.370518% | 72.501768% |

| 2008 | 78.008148% | 74.744854% | 67.495987% | 72.301570% |

| 2009 | 77.114622% | 75.420875% | 67.595960% | 70.208609% |

| 2010 | 77.075022% | 76.320711% | 68.157788% | 69.343654% |

| 2011 | 77.207691% | 77.892216% | 68.459240% | 68.967922% |

| 2012 | 77.710148% | 78.235789% | 69.161920% | 69.196894% |

| 2013 | 78.090883% | 78.625264% | 70.773639% | 69.253713% |

| 2014 | 77.444969% | 78.839200% | 71.835052% | 69.997790% |

Source: Adapted from Figure F in Josh Bivens et al., It’s time for an ambitious national investment in America’s children, Economic Policy Institute Report, April 6, 2016

Reducing gender and inequality wage gaps

and lowering unemployment enough to spur sustainable wage growth are

absolutely essential steps if we are serious about restoring economic

security to millions of working families. But a working labor market

requires more than just jobs and wages. It requires a policy

infrastructure that enables workers to enter the labor market and be

productive in their roles as employees because they don’t have to make

difficult choices between their careers and their caregiving

responsibilities.

Paid family leave and subsidized child care provide family security, which benefits employers and the economy. But there are currently no national standards regarding paid family leave or subsidized child care. Each worker is left to the whims of individual company policies, which often means no allowance or support for family leave or child care. Therefore, workers have to make difficult choices between their careers and their caregiving responsibilities precisely when they need their paychecks the most, such as following the birth of a child or when they or a loved one falls ill. The lack of these policies particularly affects women, as they currently take on the lion’s share of unpaid care work. In contrast, many of our peer nations have such policies. Not surprisingly, the United States has fallen far behind some of our international peers in the share of women who are working. The graph shows the share of women age 25–54 with a job between 1995 and 2014. While the share of prime-age women with a job rose in Germany, Canada, and Japan, in the United States it actually fell. Policies that help workers, particularly women, balance work and family could meaningfully increase women’s employment, which would also mean more earnings for families and more economic activity for the country. (See EPI’s latest investigation into child care for how progressive child care policy, in particular, can benefit families, reduce inequality, and increase economic growth.)

Paid family leave and subsidized child care provide family security, which benefits employers and the economy. But there are currently no national standards regarding paid family leave or subsidized child care. Each worker is left to the whims of individual company policies, which often means no allowance or support for family leave or child care. Therefore, workers have to make difficult choices between their careers and their caregiving responsibilities precisely when they need their paychecks the most, such as following the birth of a child or when they or a loved one falls ill. The lack of these policies particularly affects women, as they currently take on the lion’s share of unpaid care work. In contrast, many of our peer nations have such policies. Not surprisingly, the United States has fallen far behind some of our international peers in the share of women who are working. The graph shows the share of women age 25–54 with a job between 1995 and 2014. While the share of prime-age women with a job rose in Germany, Canada, and Japan, in the United States it actually fell. Policies that help workers, particularly women, balance work and family could meaningfully increase women’s employment, which would also mean more earnings for families and more economic activity for the country. (See EPI’s latest investigation into child care for how progressive child care policy, in particular, can benefit families, reduce inequality, and increase economic growth.)

{kind=link}

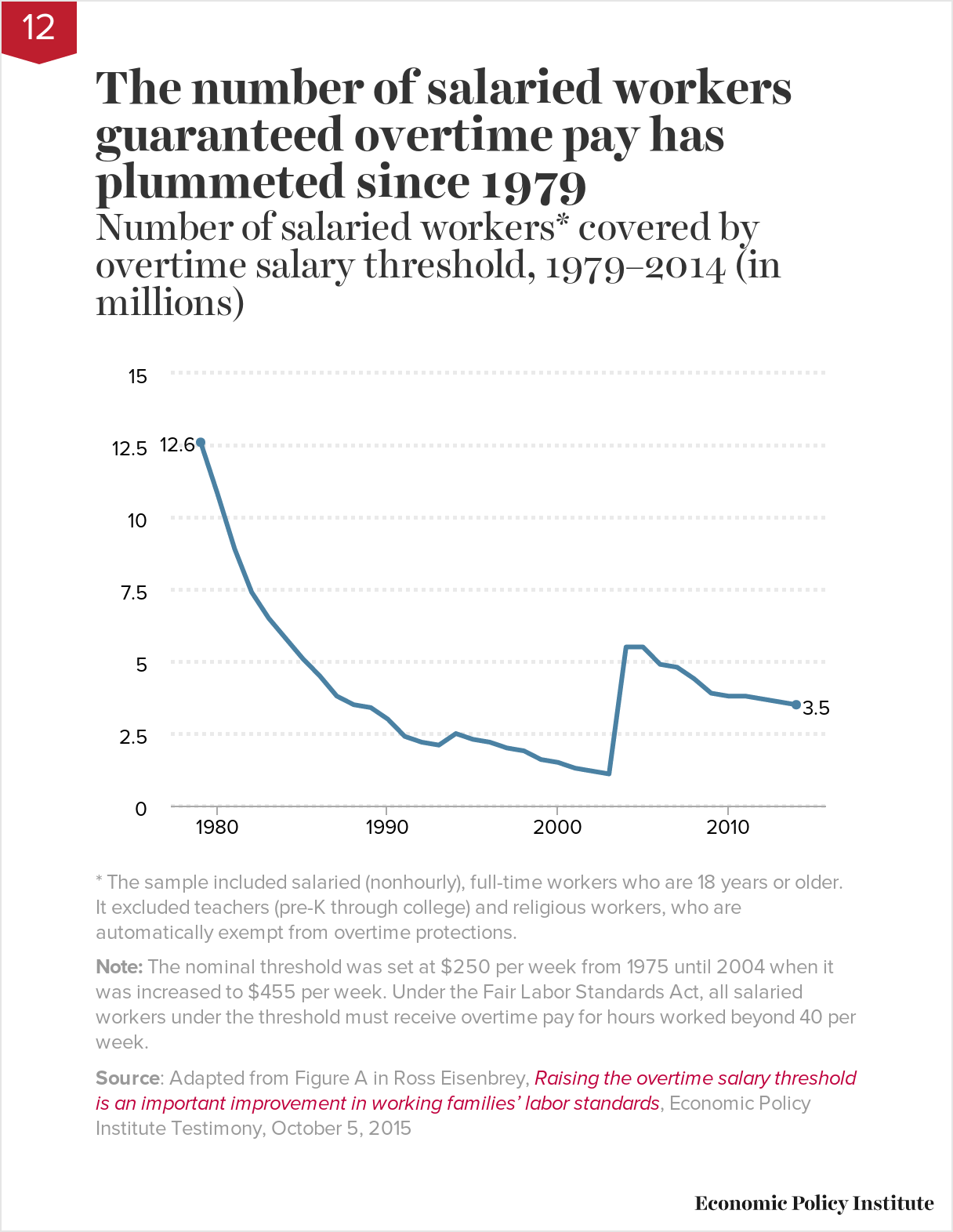

The number of salaried workers guaranteed overtime pay has plummeted since 1979Number of salaried workers* covered by overtime salary threshold, 1979–2014 (in millions)

12

| Year | Number of salaried workers* covered |

|---|---|

| 1979 | 12.6 |

| 1980 | 10.8 |

| 1981 | 8.9 |

| 1982 | 7.4 |

| 1983 | 6.5 |

| 1984 | 5.8 |

| 1985 | 5.1 |

| 1986 | 4.5 |

| 1987 | 3.8 |

| 1988 | 3.5 |

| 1989 | 3.4 |

| 1990 | 3.0 |

| 1991 | 2.4 |

| 1992 | 2.2 |

| 1993 | 2.1 |

| 1994 | 2.5 |

| 1995 | 2.3 |

| 1996 | 2.2 |

| 1997 | 2.0 |

| 1998 | 1.9 |

| 1999 | 1.6 |

| 2000 | 1.5 |

| 2001 | 1.3 |

| 2002 | 1.2 |

| 2003 | 1.1 |

| 2004 | 5.5 |

| 2005 | 5.5 |

| 2006 | 4.9 |

| 2007 | 4.8 |

| 2008 | 4.4 |

| 2009 | 3.9 |

| 2010 | 3.8 |

| 2011 | 3.8 |

| 2012 | 3.7 |

| 2013 | 3.6 |

| 2014 | 3.5 |

*

The sample included salaried (nonhourly), full-time workers who are 18

years or older. It excluded teachers (pre-K through college) and

religious workers, who are automatically exempt from overtime

protections.

Note: The nominal threshold was set at $250 per week from 1975 until 2004 when it was increased to $455 per week. Under the Fair Labor Standards Act, all salaried workers under the threshold must receive overtime pay for hours worked beyond 40 per week.

Note: The nominal threshold was set at $250 per week from 1975 until 2004 when it was increased to $455 per week. Under the Fair Labor Standards Act, all salaried workers under the threshold must receive overtime pay for hours worked beyond 40 per week.

Source: Adapted from Figure A in Ross Eisenbrey, Raising the overtime salary threshold is an important improvement in working families’ labor standards, Economic Policy Institute Testimony, October 5, 2015

Work-life balance is a fundamental goal

of the Fair Labor Standards Act (FLSA). Its requirement that employers

pay hourly and lower-earning salaried employees a premium for time

worked beyond 40 hours a week makes the FLSA the most family-friendly

law ever passed in the United States. Excessive work is detrimental to

family life, health, well-being, and productivity, and the law aims to

protect workers who are junior enough that they can be forced to work

extra hours. If not for the law’s overtime rules, tens of millions more

workers would be working 50, 60, or 70 hours a week for no additional

pay, just as millions of Americans did before the FLSA was enacted in

1938.

But millions more are still dealing with this overwork and stress on families, in part because the salary threshold that determines whether workers are automatically eligible for overtime pay is set for a 1970s economy, not a 2010s economy. As shown in the graph, in 1979 more than 12 million salaried workers earned less than the salary threshold and were therefore automatically guaranteed the right to overtime pay, regardless of their duties. Today, with a 50 percent bigger workforce, only 3.5 million salaried employees are automatically protected.

A new rule that guaranteed overtime protection to salaried workers making between $23,660 and $47,476 was instituted by the Department of Labor and was supposed to go into effect on December 1, 2016. But an egregiously bad legal decision has delayed enforcement of this common-sense rule.

But millions more are still dealing with this overwork and stress on families, in part because the salary threshold that determines whether workers are automatically eligible for overtime pay is set for a 1970s economy, not a 2010s economy. As shown in the graph, in 1979 more than 12 million salaried workers earned less than the salary threshold and were therefore automatically guaranteed the right to overtime pay, regardless of their duties. Today, with a 50 percent bigger workforce, only 3.5 million salaried employees are automatically protected.

A new rule that guaranteed overtime protection to salaried workers making between $23,660 and $47,476 was instituted by the Department of Labor and was supposed to go into effect on December 1, 2016. But an egregiously bad legal decision has delayed enforcement of this common-sense rule.

{kind=link}

It’s not technology killing manufacturing—employment was steady for 35 years between 1965 and 2000Manufacturing employment and trade deficit with China, 1965–2015

13

| Trade balance | Manufacturing employment | |

|---|---|---|

| 1965 | 0.00% | 17051 |

| 1966 | 0.00% | 17998 |

| 1967 | 0.00% | 18025 |

| 1968 | 0.00% | 18410 |

| 1969 | 0.00% | 18485 |

| 1970 | 0.00% | 17309 |

| 1971 | 0.00% | 17202 |

| 1972 | 0.00% | 18158 |

| 1973 | 0.00% | 18820 |

| 1974 | 0.00% | 17693 |

| 1975 | 0.00% | 17140 |

| 1976 | 0.00% | 17719 |

| 1977 | 0.00% | 18531 |

| 1978 | 0.00% | 19334 |

| 1979 | 0.00% | 19301 |

| 1980 | 0.00% | 18640 |

| 1981 | 0.00% | 18223 |

| 1982 | 0.00% | 16690 |

| 1983 | 0.00% | 17551 |

| 1984 | 0.00% | 18023 |

| 1985 | 0.00% | 17693 |

| 1986 | 0.04% | 17478 |

| 1987 | 0.06% | 17809 |

| 1988 | 0.07% | 18025 |

| 1989 | 0.11% | 17881 |

| 1990 | 0.17% | 17395 |

| 1991 | 0.21% | 16916 |

| 1992 | 0.28% | 16769 |

| 1993 | 0.33% | 16815 |

| 1994 | 0.40% | 17217 |

| 1995 | 0.44% | 17231 |

| 1996 | 0.49% | 17284 |

| 1997 | 0.58% | 17588 |

| 1998 | 0.63% | 17449 |

| 1999 | 0.71% | 17280 |

| 2000 | 0.82% | 17181 |

| 2001 | 0.78% | 15711 |

| 2002 | 0.94% | 14912 |

| 2003 | 1.08% | 14300 |

| 2004 | 1.32% | 14287 |

| 2005 | 1.54% | 14193 |

| 2006 | 1.69% | 14015 |

| 2007 | 1.79% | 13746 |

| 2008 | 1.82% | 12850 |

| 2009 | 1.57% | 11475 |

| 2010 | 1.82% | 11595 |

| 2011 | 1.90% | 11802 |

| 2012 | 1.95% | 11960 |

| 2013 | 1.91% | 12086 |

| 2014 | 1.98% | 12294 |

| 2015 | 2.04% | 12320 |

Note: Data

on manufacturing employment are from Current Employment Statistics

(CES) program of the Bureau of Labor Statistics (BLS). Data on Chinese

trade balance are from the Census Bureau. As a share of GDP, the

US/China trade balance was 0.00% in 1985 (first year of data

availability). We assume this value holds for pre-1985 years as well.

The presidential campaign often

highlighted the decline of American manufacturing jobs. An incorrect

conventional wisdom among economic commentators holds that the decline

of manufacturing employment has been driven by automation. This

explanation does not fit the facts. Manufacturing employment was

actually quite stable (aside from business cycle fluctuations) for 35

years between 1965 and 2000. But certainly there was plenty of

automation between 1965 and 2000. Indeed productivity growth (a proxy

for automation) was just as rapid in those years as thereafter.

But 3 million jobs were lost in the 2001–2003 recession and jobless recovery from that recession. Then rapidly growing trade deficits—particularly with China—kept the subsequent recovery from aiding manufacturing jobs. This meant that manufacturing entered the Great Recession without having regained the jobs lost in the previous recession, and in fact having lost a small number more as the rest of the economy recovered. As a result of two recessions and the “China shock,” the manufacturing sector today has nearly 5 million fewer jobs than it did in 2000.

But 3 million jobs were lost in the 2001–2003 recession and jobless recovery from that recession. Then rapidly growing trade deficits—particularly with China—kept the subsequent recovery from aiding manufacturing jobs. This meant that manufacturing entered the Great Recession without having regained the jobs lost in the previous recession, and in fact having lost a small number more as the rest of the economy recovered. As a result of two recessions and the “China shock,” the manufacturing sector today has nearly 5 million fewer jobs than it did in 2000.

No comments:

Post a Comment

One of the objects if this blog is to elevate civil discourse. Please do your part by presenting arguments rather than attacks or unfounded accusations.